Industry News

California SB 1343 Expands Sexual Harassment and Abusive Conduct Prevention Training Requirements

Author, Alyssa Burley, Client Services Coordinator, Rancho Mesa Insurance Services, Inc.

In September 2018, former California Governor Jerry Brown approved Senate Bill 1343 (SB 1343) which expands the requirements for Sexual Harassment and Abusive Conduct Prevention training within the workplace.

Editor’s Note: This article was originally published on January 17, 2019 and has been updated for accuracy on September 12, 2019.

Author, Alyssa Burley, Client Services Coordinator, Rancho Mesa Insurance Services, Inc.

In September 2018, former California Governor Jerry Brown approved Senate Bill 1343 (SB 1343) which expands the requirements for Sexual Harassment and Abusive Conduct Prevention training within the workplace.

New Requirements

Prior to SB 1343, California Assembly Bill 1825, Assembly Bill 2053, and State Bill 396, required employers with 50 or more employees to provide supervisors with sexual harassment and abusive conduct prevention training every two years. SB 1343 drops the minimum number of employees to 5 and adds a requirement for training nonsupervisory employees.

According to Senate Bill 778, passed on August 30, 2019 which expands the training deadline, “By January 1, 2021, an employer having five or more employees shall provide at least two hours of classroom or other effective interactive training and education regarding sexual harassment to all supervisory employees and at least one hour of classroom or other effective interactive training and education regarding sexual harassment to all nonsupervisory employees in California. Thereafter, each employer covered by this section shall provide sexual harassment training and education to each employee in California once every two years.”

The changes made by SB 778 not only extends the due date to January 1, 2021, but also addresses concerns about supervisory employees and clarifies when temporary workers must be trained. Read about the changes here.

Providing Training

The bills also requires the California Department of Fair Employment and Housing (DFEH), “develop or obtain two online training courses on the prevention of sexual harassment in the workplace. The course for nonsupervisory employees shall be one hour in length and the course for supervisory employees shall be two hours in length.” The department “expects to have such trainings available by late 2019,” according to a document provided by the DFEH. The online trainings are expected to be free for employers.

“In the interim period, DFEH is offering a sexual harassment and abusive conduct prevention toolkit, including a sample sexual harassment and abusive conduct prevention training. Employers may use the training in conjunction with an eligible trainer to provide sexual harassment and abusive conduct prevention training,” according to the DFEH.

An eligible trainer qualified to conduct this training would be:

Attorneys who have been members of the bar of any state for at least two years and whose practice includes employment law under the Fair Employment and Housing Act or Title VII of the federal Civil Rights Act of 1964;

Human resource professionals or harassment prevention consultants with at least two years of practical experience in:

Designing or conducting training on discrimination, retaliation, and sexual harassment prevention;

Responding to sexual harassment or other discrimination complaints;

Investigating sexual harassment complaints; or

Advising employers or employees about discrimination, retaliation, and sexual harassment prevention.

Law school, college, or university instructors with a post-graduate degree or California teaching credential and either 20 hours of instruction about employment law under the FEHA or Title VII.

Note, DFEH does not issue licenses nor certificates validating a person’s qualifications to teach sexual harassment prevention training classes.

Other training options include the online Anti-Harassment training Rancho Mesa offers to all of its clients’ supervisors and employees throughout the country in response to California’s Senate Bill 1343 (SB 1343) and Senate Bill 1300 (SB 1300).

We also can recommend Equal Parts Consulting to provide in-person supervisor and/or employee training to those in San Diego and Orange Counties. To receive a discounted rate, please let them know you are a Rancho Mesa Insurance client.

Rancho Mesa Insurance will continue to monitor training options as they become available.

For questions about this training requirement or to learn how to enroll your supervisors and employees, register for the “How to Enroll Supervisors and Employees in the Online Anti-Harassment Training” webinar or contact Rancho Mesa’s Client Services Department at (619) 438-6869.

Resources

California Department of Fair Employment and Housing. "Sexual Harassment and Abusive Conduct Prevenetion Training Information for Employers.”

https://www.dfeh.ca.gov/wp-content/uploads/sites/32/2018/12/SB_1343_FAQs.pdf

California Department of Fair Employment and Housing. “Sexual Harassment FAQs.”

https://www.dfeh.ca.gov/resources/frequently-asked-questions/employment-faqs/sexual-harassment-faqs/

Mitigating Risk at Height

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

Falls from elevated heights are the single most hazardous injury within the construction industry; representing 38% of all construction fatalities (NSC Construction & Utilities). That is a scary fact if you are a painting contractor that works off the ground. In years past, it was common to see painters working on multi-story scaffolding with few controls in place, or working from ladders on top of trucks to get those extra couple feet needed to finish a project. Workers compensation underwriters have difficulty with risks that work over 30 feet. Why is this 30 foot threshold so critical to insurance companies who write workers compensation?

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

Industry Numbers

Falls from elevated heights are the single most hazardous injury within the construction industry; representing 38% of all construction fatalities (NSC construction & utilities). That is a scary fact if you are a painting contractor that works off the ground. In years past, it was common to see painters working on multi-story scaffolding with few controls in place, or working from ladders on top of trucks to get those extra couple feet needed to finish a project. Workers compensation underwriters have difficulty with risks that work over 30 feet. Why is this 30 foot threshold so critical to insurance companies who write workers compensation?

Across the entire Construction industry, 16% of all fatal falls happened from above 30 feet (NSC Construction & Utilities).

In 2016, there were estimated to have been over 35,000 painters working in California and in total there were only 3 fatal falls (Bureau of Labor Statistics).

That accounts for less than 5% of falls, slips, or trips leading to fatality in all of California.

Mitigating Exposures: Personal Protective Equipment (PPE) and Ladder/Scaffolding Safety

As with any business that is assessing risk, start by acknowledging the potential exposures of working outside. Besides utilizing appropriate Personal Protective Equipment (PPE) for work at height, the single largest exposure for any contractor is heat exhaustion. Making sure your employees are properly hydrated and shaded is easy to overlook and can have serious consequences. Fainting at height is a serious concern and any measures that can be taken to prevent this are essential. Requiring mandatory water breaks, encouraging employees to wear loose-fitting clothes, and offering shade and protection from the sun represents tangible measures that reduce the chances of an employee suffering from heat exhaustion.

Safety equipment has become more comfortable, lighter, and easier to store and transport. Working in the heat of summer makes it difficult for employees to wear heavy equipment. This can cause them to make numerous adjustments when they are in dangerous situations. Make sure employees have light weight harnesses and are wearing them as instructed. The best PPE in the world is useless if the employees refuse to wear them properly. Similarly, it is very important to test equipment one to two times a day to ensure it is functioning properly.

Proper ladder erection and maintenance is critical for working safely at height. The recommended angle a ladder should be erected is 75 degrees. New applications such as Niosh Ladder Safety or Angel Inclination can be utilized to ensure measurements are accurate. Regular jobsite walkthroughs and inspections are also important for scaffolding. It can be fairly common that other trade contractors move or alter existing scaffolding. From day to day, objects such as connections, planks, and railing can be moved by unknown jobsite visitors and can create new fall exposures. How your safety coordinator and/or superintendents inspect and re-inspect scaffolding can literally save lives.

Turning Safe Practices into Savings

We have shared a few key tips on managing risk at height. As you design (or re-design) your fall protection program, consider how effectively your insurance broker is translating this information to the underwriters involved with your account’s renewal.

Are they clearly translating how your company mitigates risk at height?

Are they sharing key details that might separate you from another competitor?

Are they using this information to leverage competitive pricing with multiple insurance companies?

What does their information actually look like when it is sent out to an underwriter?

If these questions and this information are new to your organization, consider Rancho Mesa as an alternative. We can provide resources that can fully develop Fall Protection programs, training that can make your program actionable, and a partnership that ultimately builds the lowest cost of risk possible.

For additional information, please contact Rancho Mesa Insurance Services, Inc. at (619) 937-0164.

Reporting Serious Workers’ Compensation Injuries

Author, Jim Malone, Workers’ CompensationClaims Advocate, Rancho Mesa Insurance Services, Inc.

Workers’ Compensation injuries occur every day. The majority of these injuries are minor incidents which require no medical treatment or loss of time from work. For others, the injury is reported to the insurance carrier, the injury is addressed, forms are provided, and the recovery from the injury is monitored until the employee is released back to work and a discharge from care is provided.

Author, Jim Malone, Workers’ CompensationClaims Advocate, Rancho Mesa Insurance Services, Inc.

Workers’ Compensation injuries occur every day. The majority of these injuries are minor incidents which require no medical treatment or loss of time from work. For others, the injury is reported to the insurance carrier, the injury is addressed, forms are provided, and the recovery from the injury is monitored until the employee is released back to work and a discharge from care is provided.

However, serious injuries, illnesses or even deaths occasionally occur at work because of a work related accident. These incidents usually require 911 calls, hospitalizations, emergency surgeries, family contact, and a longer road to recovery. They may also require immediate (within 8-24 hours) reporting to the California Occupational Safety and Health Administration (Cal/OSHA), if they meet the criterion that has been established.

As defined in the California Code of Regulations Title 8 §330(h), serious injury or illness means any injury or illness occurring in a place of employment, or in connection with any employment that:

Requires inpatient hospitalization for a period in excess of 24 hours for other than medical observation.

Results in a loss of any member of the body.

Results in a serious degree of permanent disfigurement.

Results in the death of the employee.

Does not include any injury, illness, or death caused by the commission of a Penal Code violation, except the violation of Section 385 of the Penal Code, or an accident on a public street or highway.

The California Code of Regulations Title 8 §342(a) states, “every employer shall report immediately by telephone or telegraph to the nearest District Office of the Division of Occupational Safety & Health any serious injury or illness, or death, of an employee occurring in a place of employment or in connection with any employment. Immediate means as soon as practically possible but not longer than 8 hours after the employer knows or with diligent inquiry would have known of the serious injury or illness. If the employer can demonstrate that exigent circumstances exist, the time frame for the report may be made no longer than 24 hours after the incident.”

The 8-24 hour time frame begins when the employer knows, or “with diligent inquiry” would have known of the serious injury, illness, or death. The “employer” means someone in a management or supervisory capacity.

As with any injury or accident, it can be a difficult and confusing time for all those involved and affected. It may seem like many things need to be done all at once. That is, of course, impossible. So, prepare yourself now. Make a list of your responsibilities and important contact numbers before a serious injury or accident occurs.

The order in which you perform each of these responsibilities may differ, according to the type of injury or accident that occurs. However, you will still have your checklist and contact numbers ready to use to ensure you do not forget any particular step or obligation. This emergency list of telephone numbers may be your broker, safety/loss control specialist, claims administrator, or workers’ compensation claims advocate. We are all available to provide you with any assistance you may need.

For those in California, the Cal/OSHA District Office contact list is below. Ask for the officer of the day.

Concord (925) 602-6517

Oakland (510) 622-2916

San Francisco (415) 972-8670

Cal/OSHA Link: www.dir.ca.gov/title8/342.html

For additional information, please contact Rancho Mesa Insurance Services, Inc. at (619) 937-0164.

How Credit-Based Bond Programs Benefit New Contractors

Author, Andy Roberts, Account Executive, Surety Division, Rancho Mesa Insurance Services, Inc.

For small or new contractors that are looking to break into the world of government contract work, the process of getting a surety bond program in place can seem like an onerous one. It requires the contractor to compile a lot of paperwork and detailed financial reports, which can be a daunting task for any contractor, regardless of size or experience. However, there are now several “A” rated sureties that provide credit-based programs for writing smaller bonds.

Author, Andy Roberts, Account Executive, Surety Division, Rancho Mesa Insurance Services, Inc.

For small or new contractors that are looking to break into the world of government contract work, the process of getting a surety bond program in place can seem like an onerous one. It requires the contractor to compile a lot of paperwork and detailed financial reports, which can be a daunting task for any contractor, regardless of size or experience. However, there are now several “A” rated sureties that provide credit-based programs for writing smaller bonds.

The owner or owners will provide their financial information via a one or two page application, often referred to as a “fast track application.” These let you and your company apply for smaller bonds, usually $500,000 or less, depending on the surety, without requiring all the typical underwriting information that is needed to put together a formal surety program. And, so long as the owner(s) credit is good, the surety will approve the bond(s) to be issued.

These programs are great for contractors that don’t bond very often or contractors that are just starting to bid on bonded jobs. In addition, these programs also provide the contractor an opportunity to begin a relationship with a surety company, which will be very beneficial as the contractor grows and begins to bid larger bonded jobs that fall outside of the credit program, and will require a formal program with the surety.

If you have additional questions or would like to explore all the different options that each surety offers, please contact Rancho Mesa Insurance Services, Inc. at (619) 937-0166.

3 Key Differences Between Self-Insured Retention and Deductibles

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

Every business or non-profit that purchases a form of liability insurance has seen the term deductible or self-insured retention (SIR). While many know the difference between the two, many do not. Deductibles and SIRs, while quite different, are both designed to keep your premiums down. Insurers are willing to reduce the premium on policies, which have a deductible or SIR, because the insured assumes some of the risk. This however, is where the similarities end.

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

Every business or non-profit that purchases a form of liability insurance has seen the term deductible or self-insured retention (SIR). While many know the difference between the two, many do not. Deductibles and SIRs, while quite different, are both designed to keep your premiums down. Insurers are willing to reduce the premium on policies, which have a deductible or SIR, because the insured assumes some of the risk. This however, is where the similarities end.

Below are the three key differences between self-insured retention and deductibles:

With a deductible, the insured notifies the insurer when there is a claim. The insurer provides immediate defense, pays for any losses incurred and then collects reimbursement from the policyholder after the claims is closed, up to the deductible amount. Under an SIR, the insured is still required to notify the insurer of any claim. The insured will immediately begin to make payments on that claim until the SIR is satisfied. At that point, the insurer will take over.

Deductibles erode the limit of your insurance policy, while SIR(s) do not. Let’s assume you have a standard $1 million policy limit with a $50,000 deductible. In the event of a loss, the insurer will be responsible for $950,000, since the insured is required to reimburse the insurer for the full deductible amount. Under the SIR, the insured is immediately responsible for the first $50,000 of any one claim, and the insurance company is responsible for the full $1 million limit.

Large deductibles often require that the insured provide a letter of credit or some other acceptable form of collateral to cover expected losses that occur within the deductible. With SIR(s), the insurer has no responsibility for paying losses until the SIR is exhausted; therefore, no collateral is required.

When reviewing your coverages and limits, if you see the terms ‘self-insured retention’ and/or ‘deductible’ please understand the terms may seem interchangeable, but there are major differences. Please contact Rancho Mesa at (619) 937-0164 with any further questions.

Developing an Effective Injury and Illness Prevention Program (IIPP)

Author, Daniel Frazee, Executive Vice President, Rancho Mesa Insurance Services, Inc.

If you have operated a business in the state of California for any period of time, you have very likely heard about or run across the acronym IIPP. Wherever you stand with your knowledge within the world of safety, injury, and illness, it is important for every organization to understand the mandatory parts of an IIPP. What is often overlooked is how developing an effective safety program can create positive change and truly impact your bottom line.

Author, Daniel Frazee, Executive Vice President, Rancho Mesa Insurance Services, Inc.

If you have operated a business in the state of California for any period of time, you have very likely heard about or run across the acronym IIPP. Wherever you stand with your knowledge within the world of safety, injury, and illness, it is important for every organization to understand the mandatory parts of an IIPP. What is often overlooked is how developing an effective safety program can create positive change and truly impact your bottom line.

What is an IIPP?

An Injury and Illness Prevention Program (IIPP) is a required written workplace safety document that must be maintained by California employers (Title 8 of the CA code of regulations, section 3203). These regulations require eight (8) specific elements that are summarized below. In many cases, this process requires direct questions about how the company currently views and manages safety. Answering these questions will begin to highlight the positive aspects of what already is currently in place and shed light on areas that need improvement.

Responsibility

Clarifying the name, title and contact information for the person(s) with overall responsibility for the IIPP is a critical first step to this process. Making the IIPP available and accessible at all business locations becomes the first task of the “responsible person.”

Compliance

What is the content of the company’s safety meetings? Who runs those meetings? How do you discipline employees if they do not follow safety guidelines? How might the company recognize or reward their employees for safe practices or behavior?

Communication

Safety meetings are held on what type of schedule within your organization? How can employees anonymously notify management of safety and health concerns without fear of reprisal? Is there a safety committee in place that provides communication to all employees? If not, who would be considered as important members of that committee?

Hazard Assessment

Who within the company is responsible for periodic inspections to identify and evaluate workplace hazards? Provide detail on this schedule along with accompanying documentation that these visits occurred. Continuously communicating with employees for feedback and constantly reviewing hazards on a jobsite or within the workplace are crucial. Lastly, does the company use a standard or tailored JHA (Job Hazard Analysis) checklist to accomplish this? Re-visiting these checklists regularly as exposures change is critical to reducing claim frequency.

Accident/Exposure Investigation

Post-accident, who is the name of the person within the organization responsible for conducting those investigations? What type of form or checklist are you using to establish “root causes” of the accident or injury? And, back to the compliance section, what type of discipline could be handed down in the event of employee error that causes an accident or injury?

Hazard Correction

After the company has identified the hazard and determined exactly how and why an incident occurred, the IIPP must provide detail on how the company will correct the problem from happening again. One solid first step can include a review of Personal Protective Equipment (PPE) use. That is, did the equipment being used cause the accident or injury and, if yes, why? Answering the\is question may show that the piece of equipment was not appropriate for the task, or the item was defective or too old, which caused failure.

Training and Instruction

Ongoing and job specific training and instruction are really the lifeblood of any truly effective IIPP. Presenting the information in a clear, concise format that is easily understood is often the most difficult task in this process. Yet, it remains perhaps the most important as it is vital that employees are continually educated and RETAIN their instruction. Peeling back this process with managers, foreman, superintendents, etc. and learning specifically how the training is being disseminated, allows for a true baseline to be established.

Recordkeeping

Document, document, document! While establishing a written version of the IIPP might be the first step, and revising/editing on an annual basis is recommended, having the proper documentation that accompanies each section is just as important. This provides the responsible person(s) an important tool to continually compare the company’s actions, trainings, assessments and prevention techniques with the available documentation.

Can An Effective IIPP Impact my Bottom Line?

Building an effective IIPP means that the document represents a part of the company’s culture. For it to be meaningful and have a real impact on reducing workplace injuries and illnesses, it must reflect what your company is actually doing on a day to day basis. As the company’s ownership ties this into the overall business, building the IIPP from the ground up into a living, breathing document has measurable impact on controllable costs like workers’ compensation. Reducing frequency of injury can help lower the experience modification, improve the loss ratio, and establish a solid risk profile in the insurance marketplace. Having the supporting documentation along with specific examples of forms, checklists and assessments can arm an insurance broker with the tools they need in the marketplace. More specifically, this information provides a broker important leverage points when negotiating the most competitive terms possible for the employer with the insurance carrier’s underwriter. Those points can lead directly to premium savings, which leads to healthier margins and stronger profitability. Build the IIPP because it is a CA state requirement and it is the right thing to do. But, believe that building a first class safety program will absolutely lower your long-term insurance costs.

For a sample IIPP, visit the Risk Management Center or contact Alyssa Burley at (619) 438-6869.

Six Reasons for Promptly Reporting a Workers’ Compensation Claim

Author, Jeremy Hoolihan, Account Executive, Rancho Mesa Insurance Services, Inc.

Reporting workers’ compensation claims in a timely manner can have a huge impact on the severity of the claim. Some policyholders believe the practice of not reporting employee injuries early is a good business practice. This could not be further from the truth.

Author, Jeremy Hoolihan, Account Executive, Rancho Mesa Insurance Services, Inc.

Reporting workers’ compensation claims in a timely manner can have a huge impact on the severity of the claim. Some policyholders believe the practice of not reporting employee injuries early is a good business practice. This could not be further from the truth. Below are six reasons why reporting claims early can reduce the overall impact of a claim on an employer’s insurance premiums:

Lowers the cost of a claim – The cost of a claim gets higher and higher for each day it is not reported. Claims reported after 30 days of the injury on average cost 30% more than those reported right away.

Ensures that key evidence is secured – The prompt reporting of a claim allows the claims adjuster to ensure key evidence is preserved. It also ensures that the supervisor’s accident report and witness statements are taken while things are still fresh in their minds.

Potential hazards are identified as early as possible – When an injury or near miss occurs, there should be an accident investigation completed to find out the root cause of the injury. Identifying the cause or potential hazard will reduce the likelihood of a similar claim from occurring in the future. It can also be useful as a training topic during safety-related meetings.

Could identify “red flags” for fraud – It is very important to understand that an insurance company only has 90 days from the employer’s (or their management or supervisors) date of knowledge to accept or deny a claim. If the claim is reported late, it leaves the adjuster little time to investigate the validity of a claim, which might force them to accept it. If the claim is reported 90 or more days after the date of knowledge, the adjuster has no choice but to accept the claim. The impact of a fraudulent claim can have a significant effect on future workers’ compensation pricing.

Reduces litigation – When an injury claim is not reported in a timely manner by the employer, it can make the injured employee feel neglected or disgruntled. Reporting the claim early, showing compassion towards the employee, and keeping the lines of communication open will significantly reduce the likelihood of a litigated claim. Employees need to feel they are going to be taken care of medically and still have a job at the company. Employees are more likely to hire an attorney when they feel uneasy about their job security or they are not receiving proper treatment. When a claim becomes litigated, it typically prolongs the time it takes to close the claim and increases the cost by an average of 30%.

Untreated medical only injuries could develop into indemnity claims – A small percentage of medical only claims can turn into indemnity claims as a result of unforeseen complications. For example, if an employee has a small metal shard stuck in their finger and chooses not to receive treatment, the finger could become infected, require surgery, and ultimately cause nerve damage. Had this injury been properly treated from the beginning, it likely would have simply been a first aid claim. Early treatment is key to minimizing indemnity claims.

Quickly reporting claims is simply one risk management strategy to controlling a business’s insurance costs. To discuss this strategy and others please feel free to contact Rancho Mesa Insurance at 619-937-0174.

15 Tips for Reducing Exposures When Performing Median Work

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

Many city contracts and some residential communities will call for landscape contractors to install, maintain, or remodel road dividing medians. The potential risk for injury that can occur due to this exposure is highly severe. If your operations include any percentage of median work, then be sure to understand this increases your overall risk profile and slides the operations needle towards “heavy” in class.

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

Many city contracts and some residential communities will call for landscape contractors to install, maintain, or remodel road dividing medians. The potential risk for injury that can occur due to this exposure is highly severe. If your operations include any percentage of median work, then be sure to understand this increases your overall risk profile and slides the operations needle towards “heavy” in class.

Are you going above and beyond to prevent injuries from occurring as a result of your median work? Here are some quick safety tips you can implement today to better protect your employees from median work related injuries:

Eliminate median work when possible. This is the quickest way to completely separate employees from the exposure.

Consider the time of day as it relates to visibility and traffic for both vehicles and pedestrians.

Employee familiarity

Proper signage and cones

Is someone on staff trained as a competent traffic control person?

Has a Job Hazard Analysis been completed before work begins?

High visibility clothing (vests or shirts)

Employees should face oncoming traffic as much as possible when working in / near a street.

Ensure work zone buffer space is great enough to provide adequate recovery area for errant vehicles.

What is escape route in case a vehicle crosses into the work zone?

Communicate the importance of maintaining an escape route with project managers and landscaper crews.

Make modifications to temporary traffic control, if necessary.

Do not park vehicles in the buffer space.

Be aware of pedestrian traffic near work site. Is there a clear path for pedestrians to travel safely, including those with mobility issues such as the elderly or disabled?

Ensure a Heat Illness Prevention plan is in place during hot months.

Note, these are only suggestions and all may not apply to your particular exposure. Consult with a safety specialist for proper training and work site safety procedures.

For questions about how median work can affect a company’s risk profile, contact Rancho Mesa Insurance Services, Inc. at (619) 937-0164.

California Insurance Commissioner Announces Rate Cuts for 2019

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

California employers received some great news regarding their Workers Compensation premiums for 2019. On November 6, 2018, Insurance Commissioner Dave Jones recently announced his decision to cut California Workers’ Compensation advisory pure premium rates by 8.4% significantly higher than the initial recommended 4.5%. This change will affect policies that renew or incept on or after January 1, 2019.

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

California employers received some great news regarding their Workers Compensation premiums for 2019. On November 6, 2018, Insurance Commissioner Dave Jones recently announced his decision to cut California Workers’ Compensation advisory pure premium rates by 8.4% significantly higher than the initial recommended 4.5%. This change will affect policies that renew or incept on or after January 1, 2019.

To learn more about how this decrease will affect your company’s workers’ compensation premium in 2019, contact Rancho Mesa Insurance Services at (619) 937-0164.

What is a Surety Bondability Letter?

Author, Matt Gaynor, Director of Surety, Rancho Mesa Insurance Services, Inc.

When an owner or general contractor is looking to pre-qualify a contractor for a specific project, they will often request the contractor to submit a bondability letter from their bond agent. The bondability letter provides the owner with an assurance that the contractor has been underwritten and approved by a surety company for support of a specific project. The bondability letter is issued for no cost (it is regarded as a standard service provided by the bond agent).

Author, Matt Gaynor, Director of Surety, Rancho Mesa Insurance Services, Inc.

When an owner or general contractor is looking to pre-qualify a contractor for a specific project, they will often request the contractor to submit a bondability letter from their bond agent. The bondability letter provides the owner with an assurance that the contractor has been underwritten and approved by a surety company for support of a specific project. The bondability letter is issued for no cost (it is regarded as a standard service provided by the bond agent).

The typical bondability letter contains the following information:

a.) How long the bond company has been providing bonding for the contractor,

b.) The A.M. Best rating of the bond company (typically required to be “A” or above),

c.) Confirms that the bond company is on the U.S. Treasury approved list, and that the bond company is licensed in the state where the work is to be performed,

d.) Provides the single and aggregate bond limits that the bond company will support the contractor,

e.) Includes contact information of the bond agent for follow-up if the owner or general contractor has additional questions.

Although the bondability letter is non-binding and does not provide the same assurance that a bid, performance, or payment bond would provide, it is still a useful pre-qualification tool that does not require the contractor to spend any money.

If you are looking for an inexpensive way to pre-qualify your company with an owner, work with a Rancho Mesa Insurance for assistance with a bond program.

How a Medical Billings Errors & Omissions Policy Can Protect Against A Medicare Recovery Audit

Author, Sam Brown, Vice President, Human Services Group, Rancho Mesa Insurance Services, Inc.

Human Service agencies billing Medicare may find themselves paying thousands of dollars in defense costs and regulatory fines resulting from a Medicare Recovery Audit. According to the Centers for Medicare and Medicaid Services, “the Medicare Fee for Service (FFS) Recovery Audit Program’s mission is to identify and correct Medicare improper payments through the efficient detection and collection of overpayments made on claims of health care services provided to Medicare beneficiaries.”

Author, Sam Brown, Vice President, Human Services Group, Rancho Mesa Insurance Services, Inc.

Human Service agencies billing Medicare may find themselves paying thousands of dollars in defense costs and regulatory fines resulting from a Medicare Recovery Audit. According to the Centers for Medicare and Medicaid Services, “the Medicare Fee for Service (FFS) Recovery Audit Program’s mission is to identify and correct Medicare improper payments through the efficient detection and collection of overpayments made on claims of health care services provided to Medicare beneficiaries.”

The audit process can uncover medical billing errors that result in very costly penalties. Under the Civil Monetary Penalties Law, civil penalties may include an assessment of up to three times the amount claimed for each item or service. These audits are conducted by outside independent contractors and medical collection agencies, collectively referred to as Recovery Audit Contractors (RACs). The RAC firm is compensated between 9%-12.5% of the overpayments identified and recovered.

The Recovery Audit Program targets healthcare organizations, including social service agencies, behavioral health facilities, physician groups, hospitals, and billing entities.

To address this exposure to financial loss, Human Service agencies should explore a Medical Billings Errors & Omissions policy and the coverage it provides. These policies will often cover the following:

1) Defense costs and regulatory fines from actual or alleged billings errors for claims brought by:

Governmental agencies

Recovery Audit Contractors

Qui Tam Plaintiffs

Commercial Health Insurance Payers

2) Coverage for regulatory actions:

Billings error proceeding

Health insurance portability and accountability act (HIPAA)

Physician Self-Referral (STARK)

Emergency Medical Treatment and Active Labor Act (EMTALA)

To learn more about your organization’s exposure and the appropriate insurance options, please contact Rancho Mesa Insurance Services at (619) 937-0164.

Important Reminder for Janitorial Business Owners: Property Service Worker Protection Act

Author, Jeremy Hoolihan, Account Executive, Construction Group, Rancho Mesa Insurance Services, Inc.

A few of my janitorial clients have recently asked for information on the Property Service Worker Protection Act (AB 1978) and its requirements. Below is a description of the law and instructions on registering. As a reminder, the deadline for all janitorial service providers to register for the Property Service Worker Protection Act was October 1, 2018. If you have not yet registered, I would recommend doing so, as soon as possible.

Author, Jeremy Hoolihan, Account Executive, Construction Group, Rancho Mesa Insurance Services, Inc.

A few of my janitorial clients have recently asked for information on the Property Service Worker Protection Act (AB 1978) and its requirements. Below is a description of the law and instructions on registering. As a reminder, the deadline for all janitorial service providers to register for the Property Service Worker Protection Act was October 1, 2018. If you have not yet registered, I would recommend doing so, as soon as possible.

AB 1978 is a law to protect janitors against wage theft and sexual harassment. The law is designed to move the janitorial industry into a modern and transparent industry. There are three main legal mechanisms: record keeping, registration with the Labor Commissioner’s Office, and sexual harassment prevention training.

Recordkeeping

Every employer must keep the following accurate records for three years, showing all of the following:

The names and addresses of all employees who perform janitorial or cleaning services.

The hours worked daily by each employee, including the start and stop times of each work period.

The wage and hourly rate paid each payroll period.

The age of all minor employees.

Any other conditions of employment.

Registration

Every employer who provides janitorial services with a least one employee and one janitor must register with the Labor Commission. An “employer” is broadly defined as any person or entity that employs at least one employee and one or more covered workers and that enters into contracts, subcontracts, or franchise arrangements to provide janitorial services must register yearly with the Labor Commissioner’s office.

To register, an employer must pay a $500 nonrefundable application fee. The registration is valid for one year and must be renewed annually by the month and day of the original registration’s issuance. The renewal fee is also $500. A janitorial employer who fails to register is subject to a civil fine of $100 for each calendar day that the employer is unregistered, not to exceed $10,000.

The documents required to register include:

Fictitious Business Name Statement(s) (doing business as (DBA) for all business name(s) you use or intend to use.

State Employer Identification Number (SEIN) or application for it.

Federal Employer Identification Number (FEIN) or application for it.

Articles of Incorporation, if you are a corporation.

Articles of Organization, if you are a limited liability company (LLC).

Certificate of Limited Partnership, if you are a limited partnership.

Secretary of State Statement of Information, if you are a corporation or LLC.

Proof of workers’ compensation coverage via one of the following:

A valid workers’ compensation insurance certificate which must include the complete and correct name of the legal entity that is the insured employer, including fictitious business names and the complete and correct address for each location.

Certificate of authority to self-insure.

If contracting with an employee leasing company, a current workers’ compensation insurance certificate that is provided to you by the employee leasing company.

Sexual Harassment Prevention Training

The Property Service Workers Protection Act requires janitorial services employers to provide training in the prevention of sexual violence and harassment at least once every two years.

Until the training requirements are established pursuant to Labor Code section 1429.5, employers may meet this obligation by giving employees the Department of Fair Employment and Housing pamphlet DFEH–185, “Sexual Harassment,” in English or Spanish, as appropriate.

Rancho Mesa clients have access to discounted Sexual Harassment Prevention training online in both English and Spanish through the Risk Management Center. Contact Alyssa Burley at (619) 438-6869 for more information.

For more information about the Property Service Workers Protection Act, visit the Department of Industrial Relations website.

2019 Expected Loss Rates Published in California’s Updated Regulatory Filing – X-MOD Impact Inevitable for 0042 Class Code

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

The 2019 Expected Loss Rate (ELR) for Landscaping class code 0042 was recently published at a 15% decrease or $2.97.

The ELR is the factor used to anticipate a class code’s claim cost per $100 for the experience rating period. It is not to be confused with the Pure Premium Rate (PPR). The ELR differs from the PPR in that the ELR simply measures the basic claim cost for a class code without including loss adjustment expense, excess loss load (capped at $175,000 for X-MOD purposes), and loss development.

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

The 2019 Expected Loss Rate (ELR) for Landscaping class code 0042 was recently published at a 15% decrease or $2.97.

The ELR is the factor used to anticipate a class code’s claim cost per $100 for the experience rating period. It is not to be confused with the Pure Premium Rate (PPR). The ELR differs from the PPR in that the ELR simply measures the basic claim cost for a class code without including loss adjustment expense, excess loss load (capped at $175,000 for X-MOD purposes), and loss development. The PPR includes all of the mentioned above factors and is the rate for which a carrier can expect to pay for all of the cost associated with claims in a specific industry. The PPR does not account for the carrier’s overhead, profit, tax, and commissions.

Under most circumstances, when you hear the word decrease as associated with insurance its a good thing, but in the case of the ELR, a decrease will have a negative impact on your Experience MOD (X-MOD). In simple terms, if your losses stay the same and the ELR for your industry is down 15%, your X-MOD is going to go up.

At 15%, the landscape class code accounts for one of the largest swings in the 2019 regulatory filing for all industries. This only reinforces the importance of mitigating claim frequency, superior carrier claims handling, internal claims advocacy, claim cost consolidation efforts, and a proven system to keep all of these aspects running constantly. Fortunately, Rancho Mesa has a system in place today and it is a proven success.

Don’t be caught off guard in 2019; have a plan and always anticipate for the future. Let Rancho Mesa help manage your landscape insurance needs. For more information, call (619) 937-0164.

Distracted Driving, Not Just an Automobile Insurance Issue, Bad News for Workers Compensation Too

Author, David J Garcia, A.A.I, CRIS, President, Rancho Mesa Insurance Services, Inc.

I’ve written at length on the negative effects distracted driving is having on the automobile insurance industry and its impact on the rise in accidents, claim costs, and increases to your automobile premiums. But, have you considered its effects on your Experience Modification Rate (EMR) and ultimately workers’ compensation cost?

Author, David J Garcia, A.A.I, CRIS, President, Rancho Mesa Insurance Services, Inc.

I’ve written at length on the negative effects distracted driving is having on the automobile insurance industry and its impact on the rise in accidents, claim costs, and increases to your automobile premiums. But, have you considered its effects on your Experience Modification Rate (EMR) and ultimately workers’ compensation cost?

When one of your employees is injured in an automobile accident while working on your behalf, Arising out of Employment (AOE) / Course of Employment(COE) their sustained injury will be covered by your workers’ compensation policy, regardless of fault.

“Regardless of fault?!”

When a third party is deemed at fault and the injuries to your employee(s) have been settled, your workers’ compensation insurance carrier may “subrogate” their costs to the carrier representing the at fault driver. Now, here is the realty – studies have shown that 14.7% (4.1 million) of all California drivers are uninsured, while another large percentage of drivers hold the California minimum limits of $15,000/$30,000. What this means is that even if subrogation is a possibility, the likelihood of a “full” recovery is not probable. Thus, all the costs of the injury to your employee(s) will likely be the sole responsibility of your workers’ compensation carrier and this claim cost negatively affects your EMR and loss ratios for years to come.

What can you do?

You can implement a strong fleet safety program that includes a policy pertaining to distracted driving. When your employee is involved in a motor vehicle accident, adherence to your company’s accident investigation protocol is crucial. Documentation will prove pivotal for your carrier if subrogation becomes a possibility.

For our clients, through RM365 Advantage, we have a number of resources: fleet safety programs that can be customized, fleet safety training topics, fillable and printable accident investigation forms, archived fleet safety workshop videos, and more, in both English and Spanish. You can access this through our RM365 Advantage Risk Management Center or contact our Client Services Coordinator Alyssa Burley at aburley@ranchomesa.com.

If you are not a current client of Rancho Mesa, we encourage you to reach out to your broker for assistance or email Alyssa Burley to get additional information or to ask any questions.

Contractor Strategies to Maximize Your Bank Line of Credit

Author, Matt Gaynor, Director of Surety, Rancho Mesa Insurance Services, Inc.

Some of my most successful bond clients opened their construction business with a good amount of working experience on their resume, but only a minimal amount of cash and capital. Unfortunately, bond companies like to see a strong amount of cash and capital. Therefore, my goal, as their bond agent, is to work with what they have at the present time to explain why they are a “good risk” now for bid, performance, and payment bonds - along with ideas on how to overcome the initial cash and capital constraints.

Author, Matt Gaynor, Director of Surety, Rancho Mesa Insurance Services, Inc.

Some of my most successful bond clients opened their construction business with a good amount of working experience on their resume, but only a minimal amount of cash and capital. Unfortunately, bond companies like to see a strong amount of cash and capital. Therefore, my goal, as their bond agent, is to work with what they have at the present time to explain why they are a “good risk” now for bid, performance, and payment bonds - along with ideas on how to overcome the initial cash and capital constraints.

As a contractor grows and is looking at larger single and aggregate bond programs, I make it a point to work with the contractor on upgrading their financial presentation along with the goal to qualify for a Bank Line of Credit. It can sometimes be difficult to qualify for that “first” bank line of credit.

We want to help! On Friday, September, 28th, we will be inviting a local bank professional to cover "Contractor Strategies to Maximize their Bank Line of Credit." Our goal is to answer some of the following questions to prepare the contractor for a favorable submission process with the banker:

a) What is the typical information needed from the Contractor to apply for a Bank Line?

b) How do I determine what size Line of Credit I should ask for?

c) What are the “key” underwriting areas you will concentrate on?

d) How long after we provide you the information should we expect an answer?

e) To qualify for a line of credit – do we need to move our checking account to your Bank?

The seminar will allow us to pull back the curtain with the banker to make this process as seamless and painless as possible. The seminar will provide the contractor an opportunity to ask the questions you might have avoided because you assumed you did not qualify.

If interested, please register online or contact Rancho Mesa Insurance at (619) 937-0164.

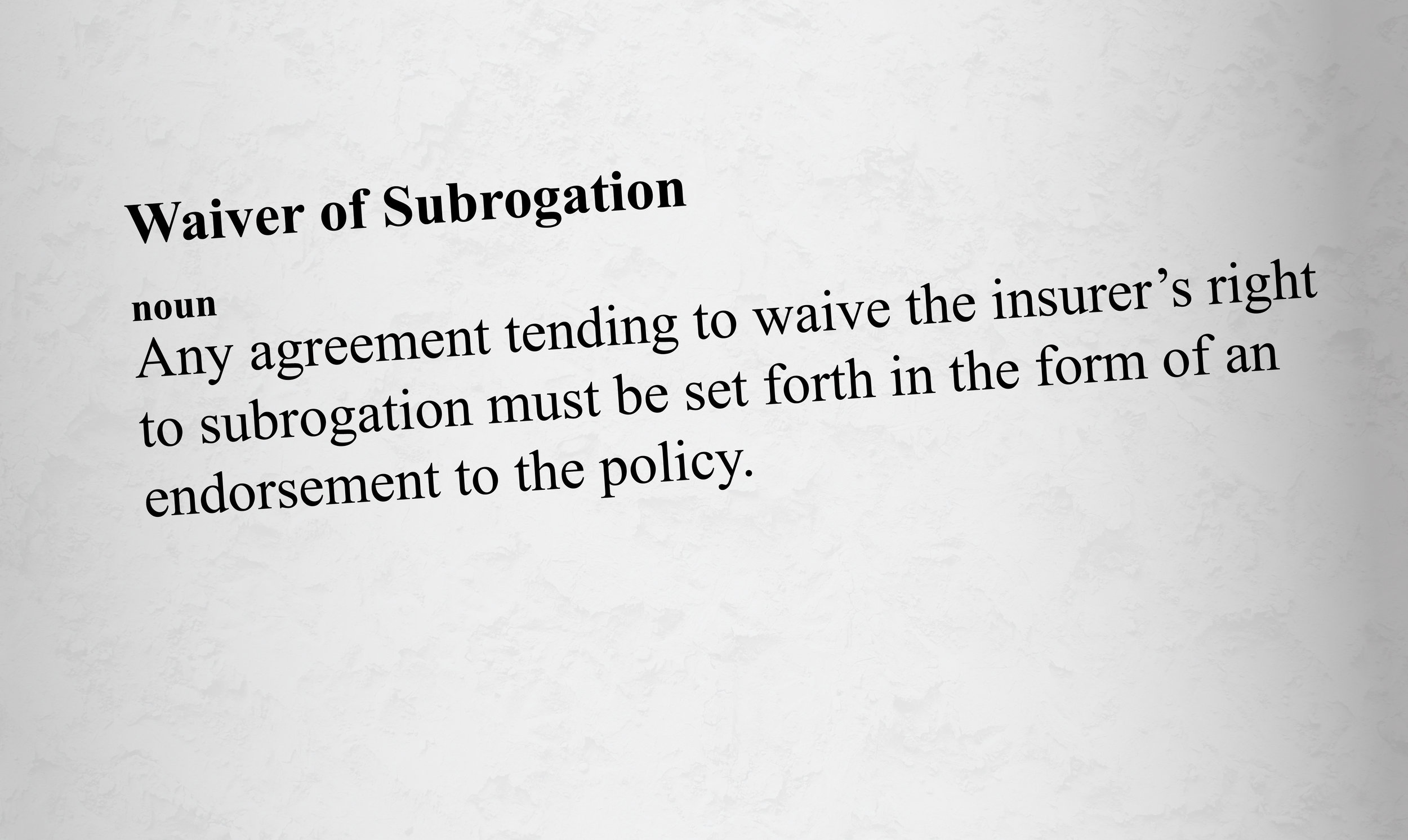

Understanding Waivers of Subrogation for Contractors

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

In an era where general contractors commonly require a Waiver of Subrogation from its sub-contractors before they are allowed to step foot on the jobsite, it is important to understand how a Waiver of Subrogation functions. Most companies simply tell their agent they need the waiver added to their contract, but what does this mean? How does it affect the policy?

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

In an era where general contractors commonly require a Waiver of Subrogation from its sub-contractors before they are allowed to step foot on the jobsite, it is important to understand how a Waiver of Subrogation functions. Most companies simply tell their agent they need the waiver added to their policy, but what does this mean? How does it affect the policy?

Subrogration is "the legal process by which an insurance company, after paying for a loss, seeks to recover all or a portion of the loss from another party who is legally wholly or partially liable for that loss," according to the Workers' Compensation Insurance Rating Bureau of California (WCIRB). So, a Waiver of Subrogration prevents your insurance carrier from recovering funds paid on a claim from the named party requesting the waiver.

When subrogating, three things must be established:

1) The defendant was negligent (or that a product was defective),

2) Negligence proximately caused the damages for which the carrier paid, and

3) The amount and nature of the damages.

If you cannot establish any one of these three, there will be no subrogation.

Subrogation is used throughout various lines of insurance. It is very common in dealing with auto insurance claims. If you are in an accident and the other driver is deemed to be at fault, your insurance company will respond first by paying to have your vehicle fixed. Then, the carrier will collect from the at fault driver’s insurance company to recover the amount they had to pay to fix your car. The insured’s carrier jumps on the claim immediately so that the insured will not have to wait for the claim to be disputed and resolved before their car is repaired. Claims are handled the same for every line of insurance, unless there is a Waiver of Subrogation in place.

When a sub-contractor is hired and has signed a Waiver of Subrogation for the project owner or general contractor, they are essentially waiving their carrier's ability to recover the money that was paid out on a claim that was caused by a third party's negligence. Waivers of subrogation often come in two formats. Either, the waiver specifically names an entity that the carrier waives its’ right to subrogate against, or a Blanket Waiver of Subrogation. If a Blanket Waiver of Subrogation is provided, the carrier must obtain permission from the named insured to subrogate against a third party.

When adding a Blanket Waiver of Subrogation to a policy, there is an additional fee to offset the carrier’s ability to reclaim money from any losses that were caused by a third party's negligence. These fees can change from carrier to carrier and it is a good move to review each policy to know exactly what you are paying for waivers. Adding a blanket waiver of insurance does not increase coverage or limits, it simply absolves an owner/general contractor of their liability.

With Waivers of Subrogation becoming more prevalent, it is easy to see how important it is as a business owner to know exactly what is covered and what you are waiving.

If you have any questions or would like to understand subrogation further, please contact Rancho Mesa at (619) 937-0164.

Update: 8868 Class Code Changes - Proposed WCIRB Changes Awaiting Public Hearing August 3rd

Author, Chase Hixson, Account Executive, Human Services Group, Rancho Mesa Insurance Services, Inc.

On August 3, 2018, the California Department of Insurance will hold a public hearing regarding the proposed changes to the 8868 Class Codes.

On August 3, 2018, the California Department of Insurance will hold a public hearing regarding the proposed changes to the 8868 Class Codes.

The proposed changes, at the recommendation of the Workers’ Compensation Insurance Rating Bureau (WCIRB), will break the 8868 class code into the following divisions:

8868 & 9101 – K-College Schools (Academic Professionals & Non-Academic Professionals, Respectively)

8869 & 9102 – Vocational Schools, Academic Professionals & Non-Academic Professionals respectively)

8871 – Supplemental Education

8872 – Social Services

8873 – Training or Day Programs for Adults

8874 – Special Education Services for Children & Youth

8876 – Community Based Adult Services

These changes, if approved, could have a significant impact on California businesses. A recent article by the Workers’ Compensation Executer, a leading news source in the insurance industry, suggest up to 25% increases in some of the proposed class codes.

Rancho Mesa has specialized in the education arena for nearly 20 years and is prepared to assist clients with this transition. If you have any questions, please contact Rancho Mesa Insurance Services at (619) 937-0164.

Three Reasons to Read Subcontractor Warranty Endorsements

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

Contractors General Liability Policies provide coverage for bodily injury and property damage for which the Named Insured is legally liable. This legal liability can result from the company’s direct operations or from other subcontractors hired by the Named Insured.

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

Contractors General Liability Policies provide coverage for bodily injury and property damage for which the named insured is legally liable. This legal liability can result from the company’s direct operations or from other subcontractors hired by the named insured.

Many general liability carriers will include some form of subcontractor warranty endorsement which establishes minimum requirements for subcontractors relative to insurance and other risk management benchmarks. At a minimum, these forms require written indemnification in favor of the named insured, certificates of insurance with additional insured wording, and specific insurance limits required by subcontractors.

These endorsements can vary widely from carrier to carrier; so, contractors may be faced with serious consequences in the event that requirements are not met. Below are three types of penalties policyholders may encounter:

- Coverage is DENIED relative to any loss resulting from the work of the subcontractors.

- Coverage is not altered, but a higher deductible or retained limit applies to any loss resulting from the work of the subcontractor. For example, should you fail to comply with the warranty, the deductible on the policy is amended from $5K to $25K.

- Coverage is not altered, but failure to comply will result in an additional premium charged at the final audit.

It is critical to have a strong contractual written transfer program in place with proper certificates of insurance from your subcontractors, regardless of the contract amount. Lean on your broker to interpret these endorsements and help negotiate the most favorable terms as you head into your renewal. Understanding these nuances can be the difference between a covered loss and an unexpected large capital expense.

For more information about subcontractor warranty endorsements, contact Rancho Mesa Insurance Services, Inc. at (619) 937-0164.

Six Reasons a Company’s Experience Modification Could be Recalculated

Author, Jeremy Hoolihan, Account Executive, Rancho Mesa Insurance Services, Inc.

Workers’ Compensation costs continue to be one of the most costly expenses for business owners in California. With recent reform, California has maintained steady rate decreases in the workers’ compensation marketplace. Unfortunately California still maintains some of the highest rates in the country, often times two to three times the nations average.

Author, Jeremy Hoolihan, Account Executive, Rancho Mesa Insurance Services, Inc.

Workers’ Compensation costs continue to be one of the most costly expenses for business owners in California. With recent reform, California has maintained steady rate decreases in the workers’ compensation marketplace. Unfortunately, California still maintains some of the highest rates in the country, often times two to three times the nations average.

Controlling insurance costs is vital to staying profitable and often times, staying in business. An important way business owners can control their insurance costs is by controlling their Experience Modification or X-MOD. An X-MOD is a benchmark of an individual employer against others in its industry, based on that employer's historical claim experience. This comparison is expressed as a percentage which is applied to an employer's workers' compensation premium.

The premium impact of a credit X-MOD (less than 1) vs a debit X-MOD (more than 1) can be significant. Business owners budget around their insurance costs. When there are unforeseen changes to their insurance costs it can have a dramatic effect. While it is rare, there are situations when an X-MOD can change in the middle of a policy term. Below are six circumstances when this could happen:

- If a claim that has been used in an X-MOD calculation is subsequently reported as closed mid policy term AND closed for less than 60% of the aggregate of the highest value, then the X-MOD is eligible for recalculation.

- In cases where loss values are included or excluded through mistake other than error of judgement. Basically, this rule takes into consideration the element of human error.

- Where a claim is determined non-compensable. Meaning the injury was determined to be non-work related.

- Where the insurance company has received a subrogation recovery or a portion of the claim cost is declared fraudulent.

- Where a closed death claim has been compromised over the sole issue of applicability of the workers’ compensation laws of California. Basically, if a person passes away at work but it was determined that the person had a pre-existing condition which caused the death, not work itself.

- Where a claim has been determined to be a joint coverage claim. This occurs mainly with cumulative trauma claims where there was no specific incident that caused an injury, but an injury that developed over time (i.e., wear and tear).

If any of the circumstances above have occurred, than a revised reporting shall be filed with the Workers’ Compensation Insurance Rating Bureau (WCIRB) and it shall be used to adjust the current and two immediately preceding experience ratings.

If you would like to discuss this topic in further detail, and learn how Rancho Mesa Insurance can audit your X-MOD worksheet for potential recalculations, please contact us at (619) 937-0164.

Top Three Benefits of Conducting an In-Home Health Care Safety Inspection

Author, Chase Hixson, Account Executive, Human Services, Rancho Mesa Insurance Services, Inc.

For many Home Health Care companies, conducting an in-home inspection on all new cases is standard practice. The intent of these inspections is to improve the quality of services offered; however, there is also an additional opportunity to improve the risk profile for those health care companies and thereby help them reduce their insurance costs.

For many Home Health Care companies, conducting an in-home inspection on all new cases is standard practice. The intent of these inspections is to improve the quality of services offered; however, there is also an additional opportunity to improve the risk profile for those health care companies and thereby help them reduce their insurance costs.

Best practices suggest that Home Health Care companies conduct safety inspections in the home for all new clients prior to having a caregiver work the case. If possible, have the caregiver(s) that will be in the home, conduct the inspection with you. Following are 3 ways inspections with an eye toward safety can help improve your risk profile.

Providing An Opportunity to Point out Safety Hazards

The most obvious outcome is the opportunity to point out safety hazards. Having two sets of eyes on the home will help to identify potential hazards such as a poorly lit staircase, an over stocked bookshelf where the caregiver might obtain supplies, a crowded kitchen, or loose carpet or rug.

Engaging the Employee as an Equal Partner in Safety

Studies show claims are less likely to occur when the employee is engaged in the safety process. For example, if the employee is involved with assessing their own hazards and determining their own safety, they are more likely follow the guidelines.

Improving your Frequency Rate

Conducting pre-case safety inspections is known to reduce the frequency of claims. It’s no surprise taking this step will positively impact the employer’s insurance premium. Not only is the likelihood of a claim reduced, the ability to react to a claim with proper corrective action increases, as well. If an accident were to occur, prior inspections will speed up the discovery process and allow the proper changes to be made, in theory, reducing the likelihood of the incident occurring again.

Conducting safety inspections in the home prior to assigning a case workers is a great way to not only benefit pricing immediately, reduce the likelihood of a claim in the future, thereby helping you to sustain favorable pricing in the future.

If you would like to learn more, or have any questions, please contact Rancho Mesa at (619) 937-0164.