Industry News

Employers Beware! Ten Red Flags You May Have a Fraudulent Workers’ Comp Claim

Author, Jeremy Hoolihan, Account Executive, Rancho Mesa Insurance Services, Inc.

Workers’ Compensation is a form of insurance providing wage replacement and medical benefits to employees injured in the course of employment in exchange for mandatory relinquishment of the employee's right to sue their employer for the tort of negligence.

Author, Jeremy Hoolihan, Account Executive, Rancho Mesa Insurance Services, Inc.

Workers’ Compensation is a form of insurance providing wage replacement and medical benefits to employees injured in the course of employment in exchange for mandatory relinquishment of the employee's right to sue their employer for the tort of negligence.

While most people would agree with the idea of a workers' compensation system, unfortunately, there are people who try to defraud it in an effort to earn an extra buck. These individuals include both employers and employees. For this article, I will focus solely on the most common workers’ compensation fraud, claimant fraud (i.e., when an employee commits the fraud).

Claimant fraud includes false claims and exaggerated claims. These claims typically involve soft-tissue symptoms, such as headaches, whiplash, or muscle strain, which are all very difficult to disprove. In order to increase the value of the claim, claimants will also include multiple body parts. The most common types of claimant fraud includes reporting fake claims, injuries not received on the job, exaggerated injuries, and claimants working for another employer while collecting benefits from an injury claim.

Claimant fraud causes extreme frustration, animosity, and can lead business owners to question all claims, including those that are legitimate. Employers can feel helpless, especially when the system gives the benefit of the doubt to fraudsters. There are, however, red flags that both employers and insurance companies can pick up on to fight against these individuals seeking easy money.

Ten Red Flags

The top ten red flags employers can look for on a possible fraudulent claims are: When the claimant;

Hires an attorney the day of the alleged injury.

Has several other family members also receiving workers’ compensation benefits.

Exhibits a strong familiarity with the workers’ comp system.

Has been disciplined several times or is disgruntled and fears termination.

Was engaged in seasonal work that is about to end.

Continues to cancel or fails to keep medical appointments or refuses a diagnostic procedure to confirm an injury.

Changes doctors when the original suggests they return to work.

Is seen working at another job while collecting total temporary disability.

Is reluctant to return to work and shows very little improvement.

Has problems with workplace relationships.

Contact me to learn strategies for combating fraudulent claims before and after it is reported.

The Changing Definition of Employee: What you need to know about SB 189

Author, Yvonne Gallagher, Landscape Division Account Manager, Rancho Mesa Insurance Services, Inc.

California State Capital Building.

State Bill 189 (SB 189) (Bradford) was recently enacted by the California State Legislature. It is intended to correct issues resulting from the passage of Assembly Bill 2883 (AB 2883) (Daly et. al) in 2017, which changed the requirements for business owners to exclude themselves from workers' compensation coverage.

Author, Yvonne Gallagher, Landscape Division Account Manager, Rancho Mesa Insurance Services, Inc.

California State Capital Building.

State Bill 189 (SB 189) (Bradford) was recently enacted by the California State Legislature. It is intended to correct issues resulting from the passage of Assembly Bill 2883 (AB 2883) (Daly et. al) in 2017, which changed the requirements for business owners to exclude themselves from workers' compensation coverage.

SB 189 is written to expand:

The scope of the exception from the definition of an employee to apply to an officer or member of the board of directors of a quasi-public or private corporation, except as specified, who owns at least 10% of the issued and outstanding stock, or 1% of the issued and outstanding stock of the corporation if that officer’s or member’s parent, grandparent, sibling, spouse, or child owns at least 10% of the issued and outstanding stock of the corporation and that officer or member is covered by a health care service plan or a health insurance policy, and executes a written waiver, as described above. The bill would expand the scope of the exception to apply to an owner of a professional corporation, as defined, who is a practitioner rendering the professional services for which the professional corporation is organized, and who executes a document, in writing and under penalty of perjury, both waiving his or her rights under the laws governing workers’ compensation, and stating that he or she is covered by a health insurance policy or a health care service plan. The bill would expand the scope of the exception to include an officer or member of the board of directors of a cooperative corporation, as specified. The bill would also expand the definition of an employee to specifically include a person who holds the power to revoke a trust, with respect to shares of a private corporation held in trust or general partnership or limited liability company interests held in trust, and would authorize that person to also elect to be excluded from the requirement to obtain workers’ compensation coverage, as specified. The bill would provide that an insurance carrier, insurance agent, or insurance broker is not required to investigate, verify, or confirm the accuracy of the facts contained in the waiver. (Legislative Counsel, 2018)

Once a waiver is signed and on file with the insurance carrier it will remain in effect until there is a written withdrawal. When changing insurance carriers a new waiver must be signed with the new carrier.

Effective 1/1/18

- Carriers were able to accept waivers up until 12/31/17 for policies issued in 2017 that weren't turned in on time and the officer exclusion is being honored from the inception of the policy and is being applied at final audit.

Effective 7/1/18

- Trusts will be eligible for officer exclusion.

- To be excluded, the required ownership percentage will change from 15% to 10%.

- An officer with 1%-9% ownership that is related to an excluded officer that owns 10% or more may also be excluded as long as they have health insurance.

- Waivers currently are required at the policy effective date. SB 189 provides a 15-day grace period from the effective date to turn in the waiver. The waiver may only be backdated 15 days.

Examples: With a 1/1/18 effective date, if the waiver is turned in and accepted by 1/15/18, the officer exclusion will be effective 1/1/18. With a 1/1/18 effective date, if the waiver is turned in and accepted by 2/15/18, the officer exclusion will be effective 2/1/18.

For specific questions about your workers' compensation policy, contact Rancho Mesa Insurance Services, Inc. at (619) 937-0164.

How To Lower Your Experience MOD by Understanding Your Primary Threshold

Author, Drew Garcia, NALP Program Director, Rancho Mesa Insurance Services, Inc.

The Experience Modifier (i.e., experience MOD, MOD, XMOD, experience modification rating, EMR) weighs heavy on the calculation of your workers' compensation premium. With a MOD rating of 1.00 signifying unity (i.e., the average for your industry), any MOD above 1.00 is considered adverse. Thus, any MOD below 1.00 is considered better than average. Higher MODs will debit the premium, resulting in higher workers' compensation premiums, while lower MODs will credit the premium, resulting in lower workers' compensation premiums.

Author, Drew Garcia, NALP Program Director, Rancho Mesa Insurance Services, Inc.

The Experience Modifier (i.e., experience MOD, MOD, XMOD, experience modification rating, EMR) weighs heavy on the calculation of your workers' compensation premium. With a MOD rating of 1.00 signifying unity (i.e., the average for your industry), any MOD above 1.00 is considered adverse. Thus, any MOD below 1.00 is considered better than average. Higher MODs will debit the premium, resulting in higher workers' compensation premiums, while lower MODs will credit the premium, resulting in lower workers' compensation premiums.

How do I decrease my MOD to lower my workers compensation premium?

A few factors can be addressed to reduce the workers' compensation premium. The most important is the primary threshold. Each individual employer has their own primary threshold that is determined by the class of business they operate and the amount of field payroll they accrue over a three year period. The primary threshold is the point at which any claim maximizes its negative impact on the MOD. You must be sensitive to this number because any open claim with paid amounts under the threshold, provides an opportunity to save points to the MOD. Once a claim exceeds paid amounts over your threshold, it no longer can negatively impact your MOD. However, you would still want to monitor and manage these claims to ensure your injured employee is being provided attentive care and to maintain knowledge of your loss experience.

Example

You’re a landscaping company and your primary threshold is $33,000. The most any claim can affect your MOD is $33,000 and the most points that any claim can add to your MOD is 13.

You have a claim open for $40,000 with paid amounts of $10,000 and reserved amounts of $30,000.

This claim will go into the calculation at $40,000 (Paid + Reserved) but because the total amount succeeds the primary threshold of $33,000, it will only show up on the rating sheet totaling $33,000 of primary loss and contribute 13 points to your MOD.

It would behoove you to analyze and monitor this open claim, because it has paid out amounts well below your primary threshold of $33,000.

If this same claim closes for a total paid amount of $22,000, the closed claim would go into your MOD at $22,000 with 8 points contributing to the MOD.

The difference between a $40,000 claim and a $22,000 claim is 5 points to your MOD, or, 5% to your premium!

Knowing your primary threshold is the most important piece of information when managing your XMOD. Fortunately, Rancho Mesa can help you manage your experience MOD by tracking your primary threshold and maintaining the other critical elements that go into establishing a sustainable low experience MOD.

For more information about lowering your experience MOD or a detailed analysis of your current MOD please reach out to Rancho Mesa.

Below is an example worksheet for Landscapers to determine the primary threshold.

| Annual Landscape Payroll | 2018 Primary Threshold | Max Points to MOD | Lowest MOD |

|---|---|---|---|

| $100,000 | $5,500 | 53 | .84 |

| $250,000 | $10,000 | 38 | .75 |

| $500,000 | $15,500 | 30 | .65 |

| $1,000,000 | $22,000 | 21 | .56 |

| $1,500,000 | $26,000 | 17 | .51 |

| $2,000,000 | $30,000 | 14 | .47 |

| $2,500,000 | $32,000 | 12 | .45 |

| $3,000,000 | $35,000 | 11 | .42 |

| $5,000,000 | $41,000 | 8 | .36 |

| $10,000,000 | $40,000 | 5 | .30 |

3 Practical Reasons for Timely Claims Reporting

Author, Jim Malone, Claims Advocate, Rancho Mesa Insurance Services, Inc.

When a work-related accident occurs, as a business owner or manager, it is our nature to want to analyze the situation in order to learn how to avoid it in the future. However, the reporting of the incident is equally as important. With the recent requirement to report first aid claims, timely reporting for all claims is recognized as being critical for a number of reasons.

Author, Jim Malone, Claims Advocate, Rancho Mesa Insurance Services, Inc.

When a work-related accident occurs, as a business owner or manager, it is our nature to want to analyze the situation in order to learn how to avoid it in the future. However, the reporting of the incident is equally as important. With the recent requirement to report first aid claims, timely reporting for all claims is recognized as being critical for a number of reasons.

Employee Morale

First and foremost, timely reporting allows for immediate care of any injuries that may have occurred as a result of the incident. It promotes prompt referral for medical evaluation, documentation of the bodily areas affected, and provides recommendations for treatment.

Promptly reporting an injury shows the injured employee, and their coworkers, that the company cares about them. When an employee knows the employer cares, they are less likely to litigate the claim, which can significantly reduce the overall cost to the employer.

Elimination of Hazards

Timely reporting can trigger the immediate assessment of the scene and cause of the accident. The initial focus is to document the area and determine if there is still an injurious exposure or condition present that may need to be addressed to prevent further incidents or injuries. Timely reporting also allows for prompt investigation of the accident and the scene of the accident, identify witnesses, secure faulty tools or equipment for safety and subrogation purposes, and to convey a sense of responsibility and concern for the employee that their safety is of extreme importance.

Prompt investigations into the cause of a near miss, accidents, and injuries can lead to an understanding of the factors that lead up to the incident. Thus, the employer has the opportunity to make changes in processes and improvements in safety in order to prevent future near miss events or accidents from occurring.

Cost Savings

Timely reporting can directly affect the overall costs of a claim. Decreased medical costs are realized when injuries are promptly assessed, allowing for treatment to start immediately. Injured employees tend to recover quickly when treatment is provided right away. Swift recoveries usually result in shorter periods of temporary total and/or temporary partial disability, fewer diagnostic studies, physical therapy visits, injections, surgeries, permanent physical limitations, work restrictions or permanent disability percentages, and lower future medical care needs. This translates into lower financial resources allocated to these claims.

The timely reporting of a claim promotes positive morale among employees; helps remove potential future hazards from the workplace and can significantly reduce overall the cost of incidents.

For more information about claims reporting, contact Rancho Mesa Insurance Services, Inc. at (619) 937-0164.

Experience Modification Factors and the Pre-Qualification Process

Author Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

As we enter 2018, government agencies, project owners and general contractors often require subcontractors to enter their pre-qualification process. Many of these entities will look closely at your Experience Modification Rate (EMR).

Author Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

As we enter 2018, government agencies, project owners and general contractors often require subcontractors to enter their pre-qualification process. Many of these entities will look closely at your Experience Modification Rate (EMR).

EMR is a numeric representation of a company’s payroll and claims history, compared to businesses in the same industry or standard industry classification. EMRs create a common baseline for businesses while allowing for a surcharge when employers' claims are worse than expected and credit when employers' claims are better than the industry average. More specifically, companies with an EMR rate of 1.00 are considered to have an average loss experience. Factors greater than 1.00 are considered worse than average, while less than 1.00 are considered better than average.

Pre-Qualification Process

In the highly competitive world of construction bidding, it has become more common that contractors can be precluded from the pre-qualification process due solely to above average EMRs. This represents an oversight as many companies have strong, well-developed safety programs, yet their EMR is holding them back. Some examples of this are:

- EMRs are lagging factors. They only factor the last three policy periods, not including the current policy period.

- EMRs can include claims that may have been unavoidable and do not represent a lack of safety (i.e. an employee is rear ended by an uninsured motorist).

- Large severity claims from smaller sized companies can impact the EMR much more negatively than a similar sized claims at a larger firm.

- The effectiveness of claims handling may vary from one insurance company to another, thus impacting certain employers when cases remain open with high reserves.

Rather than placing such a critical importance on the EMR Rate, owners and contractors designing the pre-qualification document should include frequency indicators like incident and DART Rate (i.e., days away, restricted or transferred) forms. These measuring tools incorporate current year totals and can provide up to 5 years of historical data. Incident Rate calculations indicate how many employees per 100 have been injured under OSHA rules within the specific time period. The DART rate looks at the amount of time an injured employee is away from his or her regular job. Lastly, contractors attempting to become pre-qualified should have the ability to provide a detailed explanation should their EMR exceed 100. This can include loss data, a summary of the company’s Illness and Injury Prevention Plan (IIPP) and code of safe practices, and more information on what exactly the company is doing to reduce future exposure to loss.

Given the importance of the pre-qualification process and the potential for contractors to be precluded from new opportunities to bid work, we’ve developed a “Best Practices” approach to assist companies in managing their EMR.

Managing Your EMR with Best Practices

The Best Practices approach to high EMRs includes a total claim physical, claims advocacy, and implementation of the Risk Management Center.

Total Claim Physical

The total claim physical accurately identifies your company's strengths and weaknesses, and then scores the company against others in the industry. It includes an audit of the EMR, analysis of claim frequency and severity, claim trends and determine root causes, provide quarterly claims reviews, and conduct pre-unit stat meetings.

Claims Advocacy

Utilizing a claims advocate can decrease existing claim costs, reduce excessive reserves, and expedite claim closures, which can reduce the EMR.

Risk Management Center

The Risk Management Center provides access to safety training materials and tracking, analysis of incidents and OSHA reporting, monthly risk management workshops and webinars.

For more information on managing your EMR before the pre-qualification process, contact Rancho Mesa Insurance Services at (619) 937-0164.

California Workers Compensation 2018 Annual Officer Payrolls Minimums and Maximums, Assessment Rates, and Dual Wage Thresholds Announced by WCIRB

ICW Group Insurance Company, the largest group of privately held insurance companies domiciled in California, recently released an announcement that outlines the details and is attached for your review.

ICW Group Insurance Company, the largest group of privately held insurance companies domiciled in California, recently released an announcement that outlines the details of California Workers Compensation 2018 Annual Officer Payrolls Minimums and Maximums, Assessment Rates, and Dual Wage Thresholds. The document is available for your review.

For any questions concerning the changes, please contact your Rancho Mesa service team.

"2018 Annual Officer Payrolls, CA Assessemnt Rates & Duel Wage Threshold." Insurance Company of the West.

OSHA Announces Top 10 Cited Violations for FY 2017

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

The Occupational Safety and Health Administration (OSHA) released its preliminary top 10 citation list for fiscal year 2017 at the annual National Safety Council (NSC) Congress and Expo, held in late September 2017.

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

The Occupational Safety and Health Administration (OSHA) released its preliminary top 10 citation list for fiscal year 2017 at the annual National Safety Council (NSC) Congress and Expo, held in late September 2017.

“One thing I’ve said before in the past on this is, this list doesn’t change too much from year to year,” said Patrick Kapust, deputy director of OSHA’s Directorate of Enforcement and Programs, during the expo presentation. “These things are readily fixable. I encourage folks to use this list and look at your own workplace.”

OSHA compiled the list using data collected from incidents occurring from October 2016 through September 2017.

- Fall Protection in Construction: 6,072 violations.

Frequently violated requirements include unprotected edges and open sides in residential construction and failure to provide fall protection on low-slope roofs - Hazard Communication: 4,176 violations.

Not having a hazard communication program topped the violations, followed by not having or providing access to safety data sheets - Scaffolding: 3,288 violations.

Frequent violations include improper access to surfaces and lack of guardrails - Respiratory Protection: 3,097 violations.

Failure to establish a respiratory protections program topped these violations, followed by failure to provide medical evaluations - Lockout/Tagout: 2,877 violations.

Frequent violations were inadequate worker training and inspections not completed. - Ladders in Construction: 2,241 violations.

Frequent violations include improper use of ladders, damaged ladders and using the top step. - Powered Industrial Trucks: 2,162 violations.

Violations include inadequate worker training and refresher training. - Machine Guarding: 1,933 violations.

Exposure points of operation topped these violations. - Fall Protection-training requirements: 1,523 violations.

Common violations include failure to train workers in identifying fall hazards and proper use of fall protection equipment. - Electrical-wiring methods: 1,405 violations.

Violations of this standard were found in most general industry sectors, including food and beverage, retail and manufacturing

Training materials for each of the items on the OSHA list are available within the Risk Management Center. Contact Rancho Mesa Insurance Services, Inc. at (619) 937-0164, for more information.

3 Steps to Protect Your Employees from San Diego’s Recent Hepatitis A Outbreak

Author, Alyssa Burley, Client Services Coordinator, Rancho Mesa Insurance Services, Inc.

Whether you work in the human services sector like healthcare, community outreach, or schools, or you are in the construction industry working in areas like downtown San Diego, your employees may come in contact with the Hepatitis A virus.

Author, Alyssa Burley, Client Services Coordinator, Rancho Mesa Insurance Services, Inc.

Whether you work in the human services sector like healthcare, community outreach, or schools, or you are in the construction industry working in areas like downtown San Diego, your employees may come in contact with the Hepatitis A virus (HAV).

As cities throughout San Diego County actively work to stop the spread of the recent Hepatitis A outbreak, some employers are asking how they can protect their employees who may be exposed to the virus.

According to the Center for Disease Control (CDC), the Hepatitis A virus is spread by “person-to-person transmission through the fecal-oral route (i.e., ingestion of something that has been contaminated with the feces of an infected person) is the primary means of HAV transmission in the United States.”

While the local and national media have primarily focused on the concentration of homeless and drug users who have contracted the virus, about 20% of the recent reported cases are not included in that population, according to the “Hepatitis A Outbreak in San Diego, CA” interview by Dennis Stein, linked to on the County of San Diego’s website. However, about half of the 20%, can trace their infection back to working with at risk populations. Thus, the Hepatitis A outbreak should be everyone’s concern, not just those included in the homeless population and drug users.

The “Hepatitis A vaccination is the best way to prevent the disease,” wrote Wilma J. Wooten, Public Health Officer and Director for the County of San Diego Public Health Services, in a letter to emergency responders, businesses, homeless providers and substance abuse treatment providers. While vaccination is an option to prevent infection, good hygiene is also highly effective.

Follow the steps below to help prevent the spread of the Hepatitis A virus to your employees:

1. Wash Hands

First and foremost, instruct employees to frequently wash their hands with soap and warm water after using the restroom, before eating, and after touching handrails, door handles, tools, and other surfaces that are frequently used by others.

Handwashing is “integral to Hepatitis A prevention, given that the virus is transmitted through the fecal–oral route,” according to the CDC’s website.

2. Sanitize

It may be necessary to regularly sanitize your facility or equipment. “Maintain routine and consistent cleaning of bathrooms for employees and the public, using a chlorine-based disinfectant (bleach) with a ratio of 1 and 2/3 cup of bleach to one gallon of water. Due to the high bleach concentration of this mix, rinse surfaces with water after 1 minute of contact time and wear gloves while cleaning,” suggests Wooten.

3. Educate

Awareness and education about the Hepatitis A outbreak is key to preventing the spread of the virus. Based on knowing the facts about how the virus is spread, employees may decide to wear disposable gloves, wash hands more frequently, or change the way they perform their job duties to prevent exposure.

The Risk Management Center provides a variety of training materials to Rancho Mesa clients on Hepatitis A and other bloodborne pathogens. Through online courses, training shorts, videos and other training materials, help educate your employees before there is an infection.

The County of San Diego also provides Hepatitis A information in the form of guidelines, cards, posters, videos and more.

Contact Rancho Mesa Insurance Services at (619) 937-0164 for more information.

Workers' Compensation Dual Wage Thresholds Increases for Construction Classes in 2018

Author David J. Garcia, C.R.I.S., A.A.I., President Rancho Mesa Insurance Services, Inc.

In an effort to keep you informed, so that you can begin to plan your 2018 budget, we wanted to let you know of a potential change in the dual wage classes, for many but not all, the dual wage construction class codes.

Author David J. Garcia, C.R.I.S., A.A.I., President Rancho Mesa Insurance Services, Inc.

Updated September 15, 2017 The Workers’ Compensation Insurance Rating Bureau has confirmed the following increases for the 2018 dual wage construction classifications. |

Originally published on May 12, 2017.

In an effort to keep you informed, so that you can begin to plan your 2018 budget, we wanted to let you know of a potential change in the dual wage classes, for many but not all, the dual wage construction class codes.

The Workers’ Compensation Insurance Rating Bureau is proposing increases in the wage threshold for ten different construction industry dual wage classifications and is likely to recommend an increase in an eleventh, by the time it releases its 2018 regulatory filing, next month. The proposed increases range from $1.00 to $2.00 per hour, to keep the thresholds in line with wage inflation. See the chart below for the actual changes.

Dual Wage Thresholds

| Classification | Current Threshold | Recommended Threshold | Threshold Difference | Last Changed |

|---|---|---|---|---|

| 5027/5028 Masonry | $27 | $27 | $0 | 2013 |

| 5190/5140 Electrical Wiring | $30 | $32 | $2 | 2014 |

| 5183/5187 Plumbing | $26 | $26 | $0 | 2014 |

| 5185-5186 Automatic Sprinkler Installation | $27 | $27 | $0 | 2009 |

| 5201-5205 Concrete or Cement Work | $24 | $25 | $1 | 2009 |

| 5403/5432 Carpentry | $30 | $32 | $2 | 2016 |

| 5446/5447 Wallboard Application | $33 | $34 | $1 | 2016 |

| 5467/5470 Glaizers | $31 | $31/further study | $1 | 2016 |

| 5474/5482 Painting/Waterproofing | $24 | $26 | $2 | 2009 |

| 5484/5485 Plastering or Stucco Work | $27 | $29 | $2 | 2014 |

| 5538/5542 Sheet Metal Work | $27 | $27 | $2 | 2009 |

| 5552/5553 Roofing | $23 | $25 | $2 | 2009 |

| 5632/5633 Steel Framing | $30 | $31 | $1 | 2016 |

| 6218/6220 Excavation/Grading/Land Leveling | $30 | $31 | $1 | 2014 |

| 6307/6308 Sewer Construction | $30 | $31 | $2 | 2014 |

| 6315/6316 Water/Gas Mains | $30 | $31 | $2 | 2014 |

Rancho Mesa will keep you informed should the proposed 2018 change go into effect. If you have any questions, please give us a call at (619) 937-0164.

Your Rancho Mesa Team - RM365 Advantage

3 Topics to Discuss with Vendors, Independent Contractors, and Partner Agencies Prior to Working Together

Author, Chase Hixson, Account Executive, Human Services, Rancho Mesa Insurance Services, Inc.

Recently, a non-profit client of mine asked the question: What are the steps I should take with vendors, contracted professionals and partner agencies to make sure my organization is protected should a claim arise as a result of their work? This is a common exposure to many of our clients, and there are several steps that can be taken to protect your business.

Recently, a non-profit client of mine asked the question: What are the steps I should take with vendors, contracted professionals and partner agencies to make sure my organization is protected should a claim arise as a result of their work? This is a common exposure to many of our clients, and there are several steps that can be taken to protect your business.

1. Verify the Proper Insurance is in Place

Any person/organization that you consider working with should be fully insured and able to provide you with a Certificate of Insurance, which lists the coverages, carriers and limits of insurance they have in place. Without their own insurance in place, your company is now assuming full responsibility for anything that may occur as a result of their negligence. Depending on the nature and scope of the work being performed, different types of insurance will be required. An insurance professional can help you determine the specific coverage needed.

Example: A charter school has hired a local animal shelter to bring animals to their students and teach about conservation. One of the animals bites a student. If the animal shelter does not have the proper insurance, the charter school’s insurance will be liable for any action taken against the school.

2. Name Your Business as Additional Insured

In addition to verifying that the correct coverages and limits are in place, you should also require they name your company as an additional insured on their policy. By doing this, your organization will now be indemnified under their policy for claims arising as a result of their work, in which you are named.

Example: In the example where a charter school has hired a local animal shelter to bring animals to their students and one of the animals bites a student, by requiring the animal shelter to name the charter school as an additional insured, the school is covered under the animal shelter’s insurance.

3. Provide a Waiver of Subrogation

A waiver of subrogation means an insured (and their insurance company) are waiving their right to subrogate against another party, should their employee suffer an injury on your premises. Most independent contractors aren’t required to carry insurance, so this wouldn’t apply to them. However, if employees of another company are performing work on your premises, it is wise to have them waive their right to subrogate against your workers’ compensation carrier.

Example: A charter school has hired a local animal shelter to bring animals to their students and teach about conservation. While presenting, an employee of the shelter trips and injures their knee. A waiver of subrogation would void the animal shelter’s workers’ compensation provider from seeking subrogation against the charter school’s workers’ compensation policy. The employee will still be treated, but you won’t suffer the penalty for it.

I strongly recommend reviewing your processes regarding vendor, independent contractors and partner agencies to see what is currently in place. Far too often steps are skipped and businesses are unaware of the liability they are assuming. If you have any question about a specific circumstance, please don’t hesitate to give Rancho Mesa a call at (619) 937-0164, we are happy to assist.

5 Steps to Avoiding Workers’ Compensation Claim Litigation

Author, Jeremy Hoolihan, CRIS, Janitorial Group Leader, Rancho Mesa Insurance Services, Inc.

Workers’ Compensation claims can cost a company time, money, employee productivity, and morale. Litigation is one of the most costly results of a workers’ compensation claim. Once an employee hires an attorney, the time and money it takes for the claim to close drastically increases.

Author, Jeremy Hoolihan, CRIS, Janitorial Group Leader, Rancho Mesa Insurance Services, Inc.

Workers’ Compensation claims can cost a company time, money, employee productivity, and morale. Litigation is one of the most costly results of a workers’ compensation claim. Once an employee hires an attorney, the time and money it takes for the claim to close drastically increases.

There are several reasons why an employee will find the need to hire an attorney. Practicing a sound Risk Management Program can dramatically reduce the likelihood of litigation. Here are some ways you can prevent most workers’ compensation claims from ever reaching that point:

- Acknowledge why employees hire attorneys. The employee/employer relationship is a critical factor in determining if a workers’ compensation claim results in litigation. Employees who feel threatened in some way are more likely to hire an attorney. A few key reasons are:

a. The employee is concerned they will be fired because of the injury and/or ownership or management doesn’t truly feel the injury was work related.

b. The employee feels they will face retaliation for reporting the claim.

c. There is a lack of understanding of the workers’ compensation claim process. For those employees that are faced with a workers’ compensation injury, it can be a very stressful time.

d. There is a fear the claim will be denied or they will be treated unfairly. Attorneys can prey on vulnerable injured employees. Radio and television ads imply injured employees need their assistance in order to get proper treatment and/or a huge settlement they deserve.

- Keep lines of communication open with your employee. Reassure the employee that he or she will have a job when they are able to return to work. In addition, show some compassion and stay in regular contact with the individual. An employee is far more likely to hire an attorney if they are concerned about losing their job or no longer of value to the company.

- Consider the ramifications before firing an injured employee. Termination of an employee after they have been injured on the job can put the company at risk of a lawsuit (Section 132 claim). In addition, terminating an injured worker could cost the company more in wage loss benefits; an injured employee will continue to draw from the workers’ compensation policy if they are unable to return to work, regardless if the company continues to employ them or not. Often, employees are released to modified duty (Return To Work Program). If an employer can accommodate the work restrictions, the employee’s temporary benefits are reduced or eliminated. This can significantly reduce the total cost of the claim.

- Act before a problem employee becomes injured. Once an injury has been reported, it becomes extremely risky to discipline or terminate a problem employee. Address and deal with the employee immediately and be consistent with your documentation.

- Train your supervisors!!!! It is vital that supervisors are trained in reporting and handling claims. They are your first line of defense in preventing claim litigation. Businesses should have a formalized Accident Investigation Program in place. Rancho Mesa provides a Supervisor’s Report of Accident or Near Miss form and a Witness’ Accident Statement form to assist in the investigation process. In addition to all the formal documentation, there are other key strategies a supervisor can use:

a. Do not accuse the injured employee of fraud, even if you know fraud is involved. Supervisors should simply document the facts. If there is suspicion of fraud, make sure you document any supporting evidence in the report and inform the adjuster.

b. Do not negotiate the injured worker’s treatment or return to work schedule. Leave that determination to the claims adjuster.

c. Keep in touch. Instruct the supervisor to check on the injured worker from time to time. Show some compassion and build trust. Assure the employee that their job is secure.

While there is no surefire way to eliminate litigated claims, by following these five steps you should see results. With the average litigated claim costing 30% more than a non-litigated claim, the savings over time could be significant. To discuss implementing this strategy within your company’s Risk Management Program, please contact Rancho Mesa Insurance Services, Inc. at (619) 937-0164.

DHS Alerts OSHA of Possible Electronic Reporting Security Breach

Author, Alyssa Burley, Client Services Coordinator, Rancho Mesa Insurance Services, Inc.

On August 1, 2017, the Occupational Safety and Health Administration (OSHA) launched its online electronic data filing application. It was designed to collect and publish injury data on companies throughout the United States in order to comply with a new requirement.

Author, Alyssa Burley, Client Services Coordinator, Rancho Mesa Insurance Services, Inc.

On August 1, 2017, the Occupational Safety and Health Administration (OSHA) launched its online electronic data filing application. It was designed to collect and publish injury data on companies throughout the United States in order to comply with a new requirement.

Within just a few weeks of its launch, according to an OSHA spokesperson, the United States Department of Homeland Security’s Computer Emergency Readiness Team alerted OSHA of a possible data breach within the newly launched Injury Tracking Application (ITA).

The warning indicated user information for the tracking application system could have been compromised and the affected company was notified about the apparent breach.

According to a Department of Labor official on August 14, 2017, “Access to the ITA has been temporarily suspended as OSHA works with the system developer to examine the issue to determine the extent of the problem.”

As of today, August 23, 2017, OSHA’s ITA webpage displays an “Alert: Due to technical difficulties with the website, some pages are temporarily unavailable,” preventing anyone from uploading their data.

In an article published by Business Insurance, legal experts were cited as advising companies to wait to file their reports. “I’m not advising anybody to file it before Dec. 1 because it might change,” said Mark Kittaka, a Columbus, Ohio-based partner with Barnes & Thornburg L.L.P. “I don’t know why you’d want to file it early. You may not have to file it all.”

However, Rancho Mesa Insurance Services advises its clients to continue to keep track of their incidents in the Risk Management Center, regardless of what happens with the OSHA electronic reporting requirement. Companies will still need to maintain current OSHA logs, even if the electronic system is unavailable or the electronic reporting requirement changes. If the December 1, 2017 deadline remains in effect, clients will be prepared to submit the data via the Risk Management Center, if the data has been maintained.

Contact Rancho Mesa Insurance Services at (619) 937-0164 if you have questions about how to track your incidents in the Risk Management Center and generate the required OSHA logs.

Congratulations, You’ve Won the Construction Contract – Now, you Need USL&H

Author, Kevin Howard, CRIS, Account Executive, Rancho Mesa Construction Group

If the title of this article gave you a good chuckle, you most likely have bid a job somewhere near a body of water; then, found out you need U.S. Longshore and Harbor (USL&H) Workers’ Compensation coverage. You were surely not the first one to overlook this requirement and you definitely will not be the last.

Author, Kevin Howard, CRIS, Account Executive, Rancho Mesa Construction Group

If the title of this article gave you a good chuckle, you most likely have bid a job somewhere near a body of water; then, found out you need U.S. Longshore and Harbor (USL&H) Workers’ Compensation coverage. You were surely not the first one to overlook this requirement and you definitely will not be the last.

History of USL&H

Let’s begin with a USL&H history lesson to understand why it was implemented, nearly 100 years ago.

The U.S. Longshore and Harbor Workers’ Compensation Act was implemented in 1927 to provide compensation to an employee if an injury or death occurred upon navigable waters of the US - including any adjoining pier, wharf, dry dock, terminal, building-way, marine railway or other adjoining area customarily used by an employer in loading, unloading, repairing, dismantling or building a vessel.

The act’s passage compensated maritime workers, including most dock workers and ship builders that were not covered by the Jones Act ( 46 U.S.C. 30004), which only covered seamen, not those who worked in maritime-support industries. Therefore, USL&H workers' compensation was intended to protect those employees who would otherwise not be covered.

Moving forward to present day, to avoid conflict, project owners and general contractors alike require subcontractors and vendors to provide USL&H coverage if projects are close to navigable waters.

Does Every Insurance Carrier Offer USL&H Coverage?

The answer is no. Not every workers' compensation carrier is filed to offer USL&H. Depending on the industry, classification codes and payroll size, there is most likely only a handful of options available. With that said, it’s important to know who those insurance carriers are if you plan on bidding a project that requires USL&H.

Acquiring USL&H Coverage

The first move to acquiring a USL&H policy is to call an insurance representative that has experience in this area. Then, you can develop a game plan that will help you navigate within the USL&H marketplace.

As an eleven-year Best Practices Agency, Rancho Mesa can assist with your USL&H needs. We have been helping clients in the construction field for over 20 years. Contact Rancho Mesa at (619) 937-0164 for more information about this type of policy.

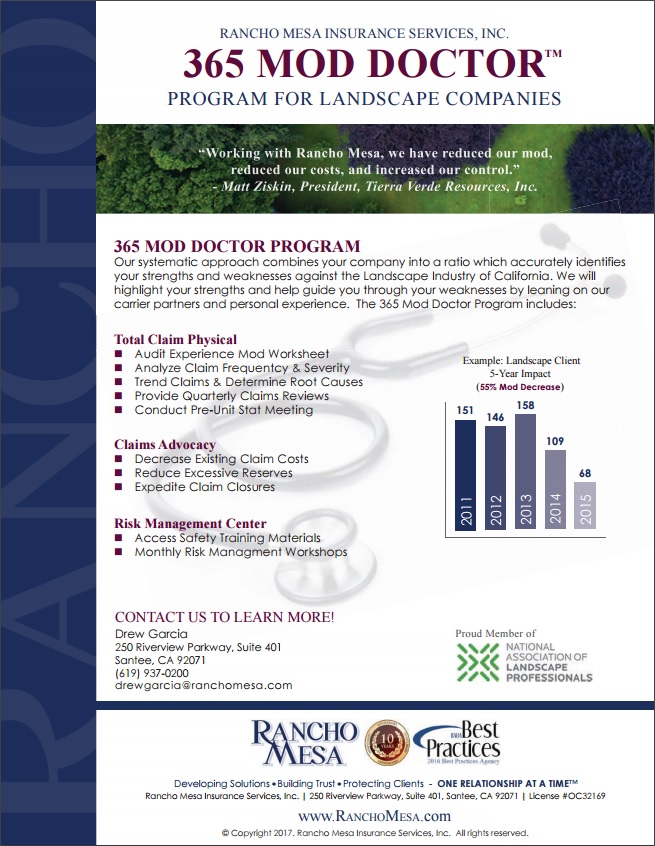

Control your Experience MOD through the MOD Doctor Process.

Author, Drew Garcia, NALP Program Director, Rancho Mesa Insurance Services, Inc.

Successfully maintaining low and predictable workers' compensation costs is a product of establishing a routine that constantly “checks and balances” your all-encompassing insurance program. Our "MOD Doctor" technique lays out a road map so we can guide you throughout the year to gain more control, become more efficient, and ultimately drive down your insurance cost; at no extra expense. What can you expect from this process?

Author, Drew Garcia, NALP Program Director, Rancho Mesa Insurance Services, Inc.

Successfully maintaining low and predictable workers' compensation costs is a product of establishing a routine that constantly “checks and balances” your all-encompassing insurance program. Our MOD Doctor™ technique lays out a road map so we can guide you throughout the year to gain more control, become more efficient, and ultimately drive down your insurance cost; at no extra expense. What can you expect from this process?

Audit Experience MOD Worksheet. Our team analyzes your experience MOD worksheet to ensure the information is accurate with payrolls, claim information, and class codes.

Analyze Claim Frequency, Severity, and Trends. It’s important to analyze your company’s loss information and specifically look for trends in order to prevent further claim activity with similar causes. Furthermore, we compare your loss experience against the landscape industry, in your state, to determine whether you are outperforming or underperforming your industry.

Claims Meetings. The largest companies maintain claim review meetings on a consistent basis. We bring this service to you and adjust the frequency of the meeting to fit your needs. It’s important to have updated information on your open claims, without sacrificing your time or your employee’s time tracking down this data.

Pre-Unit Stat. Your experience MOD is calculated on claims information which is sent into the governing bureau roughly six months into your policy period. Knowing this information, we can accurately project your MOD six months in advance giving you the information you need to begin budgeting for future work,while considering where your insurance cost will be headed.

Claims Advocacy. Our team is your advocate in helping to seek information on your claims, both in the current year and in the past. Our goal through this process is to decrease existing claim costs, reduce excessive reserves, and expedite claim closure, all while considering your unit stat date.

Risk Management Center. We know maintaining up to date and accurate information for tailgate topics, safety procedures, and incident tracking is important. The Risk Management Center streamlines these functions by making them accessible to our clients online.

Contact our Rancho Mesa staff to learn more about how the MOD Doctor can help you control your workers' compensation costs.

Uninsured and Underinsured Motorists Coverage - Are Your Limits Adequate? - Be Careful!

Author, David J. Garcia, A.A.I., CRIS, Rancho Mesa Insurance Services, Inc.

Earlier in the year, we published the article "Commercial Auto Premiums Are Rising - What’s Driving the Increases?," which addresses how insurance companies are all experiencing adverse loss experience within their commercial automobile books of business. The result of these mounting losses is causing a dramatic rise in commercial Auto premiums for most policyholders.

Author, David J. Garcia, A.A.I., CRIS, Rancho Mesa Insurance Services, Inc.

Earlier in the year, we published the article "Commercial Auto Premiums Are Rising - What’s Driving the Increases?," which addresses how insurance companies are all experiencing adverse loss experience within their commercial automobile books of business. The result of these mounting losses is causing a dramatic rise in commercial Auto premiums for most policyholders.

As a result of this trend, we are seeing many carriers and brokers reducing coverage limits and terms on certain lines of automobile coverage. This represents a major concern for any business owner that has any size fleet of vehicles. Reducing limits and/or modifying terms of coverage simply transfers more claim exposure directly to the business owner. And, unfortunately, in many cases, business owners are unaware of the change or ill informed.

One specific line of coverage that we are seeing this occur, and creates great concern, is uninsured/underinsured motorist coverage. The number of uninsured motorists nationwide is alarming and here in California there are between 3.6 million and 4.1 million uninsured drivers, or 14.7 percent of all drivers. Additionally, the minimum limit of insurance in California is only $15,000. So, while many motorists may have insurance, they are woefully “underinsured.” These factors pose potential catastrophic exposures to any business. To illustrate this point, we will briefly define these coverage’s and then look further into how these lower limits of coverage terms may impact the health of your business.

Uninsured Motorists Coverage

Uninsured Motorist Coverage (UM) helps pay your, your employees and your passenger’s medical expenses, lost wages and related property damages if you're in an accident caused by a driver who doesn't have liability insurance.

Underinsured Motorist Coverage

Underinsured Motorist Coverage (UIM) helps pay your, your employees and your passenger’s medical expenses, lost wages, and related property damages, if any of you are hurt in a car accident caused by someone with liability insurance, but whose coverage limits are lower than those you choose for this coverage, and aren't high enough to pay the damages.

Best practices suggests anything less than $1,000,000 limit for uninsured/underinsured coverage is inadequate and puts the business at extreme financial risk. Let me explain by sharing just two, of many real-world, examples of how this could occur. The following examples assume the accident is the fault of an uninsured or underinsured driver:

Example 1. If one of your employees is involved in an automobile accident by either an uninsured or underinsured motorist and it involved the use of a vehicle for business purposes, the resulting medical and indemnity costs would be covered under your company’s workers' compensation policy. Two negative consequences to your overall insurance program develop as a result of this incident. First, your workers' compensation claims experience (loss ratio and EMR) will be negatively impacted. Second, since the “at fault” driver is either uninsured or underinsured, subrogation (or the recovery of the claim dollars from the responsible party) is ruled out as a viable option to your workers' compensation carrier.

Therefore, the auto loss described above would not only negatively affect your auto insurance experience but also your workers' compensation experience, as well. By having a minimum of $1,000,000 UM/UIM limits, you would have allowed you workers' compensation carrier to subrogate the costs of the claim to the auto carrier and thereby reduce the impact to your workers' compensation loss ratio and EMR

Example 2. Let’s assume you have a non-employee in the vehicle and they are involved in an accident involving an uninsured/underinsured motorist and they are injured. Since this is a non-employee, their injuries would not be eligible for coverage under your workers' compensation policy and rest solely on your automobile insurance limits and coverages. Thus, these injuries, once the uninsured/underinsured limit of your automobile policy is exhausted, would become the responsibility of the business. By having a minimum of $1,000,000 UM/UIM limits, you would fill the gap created by the uninsured/underinsured motorist's lack of coverage and protect your business from this catastrophic loss.

These examples have only touched on the medical and indemnity portion of the loss. Consider there may be property damage involved as well, which only further increases the potential of out of pocket expenses a business might be responsible for paying. Additionally, keep in mind that any excess liability policy you may have in place does not cover uninsured/underinsured motorist claims.

In summary we recommend that you review your coverage limits and terms for adequacy concerning these critical coverages. At a minimum, you should have a limit of no less than a $1,000,000 for these coverages. The premium savings by lowering this limit or modifying its coverage terms is insignificant to the catastrophic loss you are exposing your business to. Do not allow one terrible incident to take your business from you when the cost to transfer this risk is marginal.

If you have any questions or need help in accessing your exposures, please call our Rancho Mesa Team. We offer full policy audits as part of our RM365 Advantage Program that helps you to identify any gaps in coverage and provide you with Best Practices risk management recommendations.

Timely Claim Reporting Lowers Work Comp Claims Costs and Improves Your Bottom Line

Author, David J. Garcia, A.A.I., CRIS, President, Rancho Mesa Insurance Services, Inc.

Studies have shown, by reporting your workers compensation claims in a timely basis, not only will your injured employee receive better medical treatment, it will boost company morale. Both the injured worker, as well as other employees, will see your sincere concern for their wellbeing. In addition, timely reporting practices will also improve your risk profile through reducing the overall cost of the claim, which leads to lower loss ratios and lower experience modifiers, thus, resulting in lower premiums and improvement in your bottom line.

Author, David J. Garcia, A.A.I., CRIS, President, Rancho Mesa Insurance Services, Inc.

Studies have shown, by reporting your workers compensation claims in a timely basis, not only will your injured employee receive better medical treatment, it will boost company morale. Both the injured worker, as well as other employees, will see your sincere concern for their wellbeing. In addition, timely reporting practices will also improve your risk profile through reducing the overall cost of the claim, which leads to lower loss ratios and lower experience modifiers, thus, resulting in lower premiums and improvement in your bottom line.

The following are four areas that support the early and timely reporting of claims:

- Manage Claims More Efficiently Reporting a claim quickly allows the claims examiner:

- To determine whether or not the claim is compensable.

- To meet state regulations that prohibit denial of claims after a specified time period.

- To secure appropriate treatment for the injured worker.

- To conduct an investigation and determine if fraud is suspected.

- To receive timely witness statements and pictures of the incident.

- Keep The Claim Costs Down – Improve Loss Ratio – Improve Experience Modifier Delayed reporting can significantly increase workers’ compensation claim costs, according the National Council on Compensation Insurance.

- Claims reported after 2 weeks of occurrence are 18% more expensive than those reported within 1 week of occurrence.

- Claims reported after 3-4 weeks of occurrence are 30% more expensive than those reported within 1 week of occurrence.

- Claims reported 1 month of occurrence are 45% more expensive than those reported within 1 week of occurrence.

- Most significantly, back injuries, as a group, are 35% more expensive if not reported within the first 7 days post-injury.

- Reduce Litigated Claims

- 47% of all claims reported after 4 weeks become litigated, which on average increase claims costs by 30%.

Source: NCCI’s Detailed Claim Information data for Report Years 2010 and 2011 case incurred losses valued as of 18 months after report date; not developed to ultimate - Close Claims Faster

- 50% of claims that are reported within the first two weeks close within 18 months.

- Only 29% of claims that are reported more than a month after the accident close within the same timeframe.

Source: NCCI’s Detailed Claim Information data for Report Years 2010 and 2011 case incurred losses valued as of 18 months after report date; not developed to ultimate.

| Reporting (Lag) Time | Expense Increase |

|---|---|

| 2 Weeks | 18% |

| 3 Weeks | 29% |

| 4 Weeks | 31% |

| 4 Weeks | 31% |

| 5 Weeks | 45% |

If you’re not currently reporting your claims timely, we strongly encourage you to adopt this “Best Practice” and make it a part of your company’s overall risk management program. Reporting your claims on a timely basis will get your injured employee the proper treatment quicker, provide your carrier the controls they need to manage the claim effectively, improve your risk profile, and lower your insurance costs.

What is SB 562 all about?

It may be of interest, if not importance, for all Californians to know about current proposed legislation, sponsored by Senator Ricardo Lara of Bell Gardens and Senator Toni Atkins of San Diego. The proposed bill would significantly expand the role of the state government within the healthcare system, by essentially establishing a single-payer system.

It may be of interest, if not importance, for all Californians to know about current proposed legislation, sponsored by Senator Ricardo Lara of Bell Gardens and Senator Toni Atkins of San Diego. The proposed bill would significantly expand the role of the state government within the healthcare system, by essentially establishing a single-payer system.

Under Senate Bill 562 (SB 562), the State would cover all medical services for every resident regardless of income or immigration status, including inpatient, outpatient, emergency, dental, vision, mental health, and nursing home care. Furthermore, insurers would be prohibited from offering benefits that cover the same services, potentially resulting in their choice to exit the marketplace. While the proposed bill touts that the program would eliminate co-pays and deductibles, and the need to obtain referrals, there is no mention of how it would be funded, except through “broad-based revenue.”

Obviously, many people ask me about the direction healthcare is headed in California and the Country; to which, I do my best to eliminate my interest in the subject since I make my living guiding companies through the insurance process. But, I do offer up some food-for- thought in terms of evaluating such a proposal, including citing the increasing shortfall of funding for Medicare, and the VA as examples of government-run healthcare, as it seems to me the former is going to require an eventual increase in payroll taxes, which effects everyone, employers and employees alike, and the latter is a good example of inefficiency and lack of innovation when there is no competition.

Personally, I believe that healthcare is both a right and a responsibility. As out-of-whack as the current system seems, or let’s face it, is, I just don’t know how we go about funding such a proposal without breaking the proverbial bank. The financial and economic realities have to be weighed with the politics, which is why it’s a bit of a relief that Governor Jerry Brown has asked the question in return, “Where do you get the extra money? This is the whole question?”

Whatever my thoughts, it is certainly a complex and vexing economic, social, and political issue for our times, one that will continue to be hotly debated and legislated, so there is much more to come.

Should Union Janitorial Employers have a lower Workers’ Compensation rate than Non-Union Employers?

Author Jeremy Hoolihan, CRIS, Janitorial Group Leader Rancho Mesa Insurance Services, Inc.

A recent study by the Commission on Health, Safety and Workers’ Compensation made an argument that the janitorial industry should be split into two workers’ compensation class codes. This change would be similar to how many construction operations field class codes are separated between an over and under dollar amount per hourly wage. As an example, an electrical contractor’s field wages are split at over and under $30/hour.

Author Jeremy Hoolihan, CRIS, Janitorial Group Leader Rancho Mesa Insurance Services, Inc.

A recent study by the Commission on Health, Safety and Workers’ Compensation made an argument that the janitorial industry should be split into two workers’ compensation class codes. This change would be similar to how many construction operations field class codes are separated between an over and under dollar amount per hourly wage. As an example, an electrical contractor’s field wages are split at over and under $30/hour. Why does this matter? It matters, because the workers’ compensation marketplace perceives the higher-wage-earner to be a safer risk (the thinking being - a higher-wage-earner is more experienced and less likely to sustain injury), thus, the workers' compensation premium rates are less for those in the “above” threshold category. However, the BIG difference between this rationale and the study is that rather than basing the split rates on pay scale, the study proposes the split be between Union and Non-Union companies.

The study’s line of reasoning is that Union firms have fewer injuries and as a whole have a much lower loss ratio than Non-Union firms. However, many industry experts disagree and believe that the figures are skewed and not representative of the true industry experience. Clearly with the varying opinions and so much at stake, much more research and discussion needs to take place before anything is implemented.

With that said, in order to remain relevant and competitive, all janitorial companies need to stay well informed and be prepared for any changes should they occur. Rancho Mesa’s janitorial department will keep a close eye on any new developments and continue to help improve your company's risk profile, so you will be well informed and prepared for any changes. If you have any questions please feel free to contact us

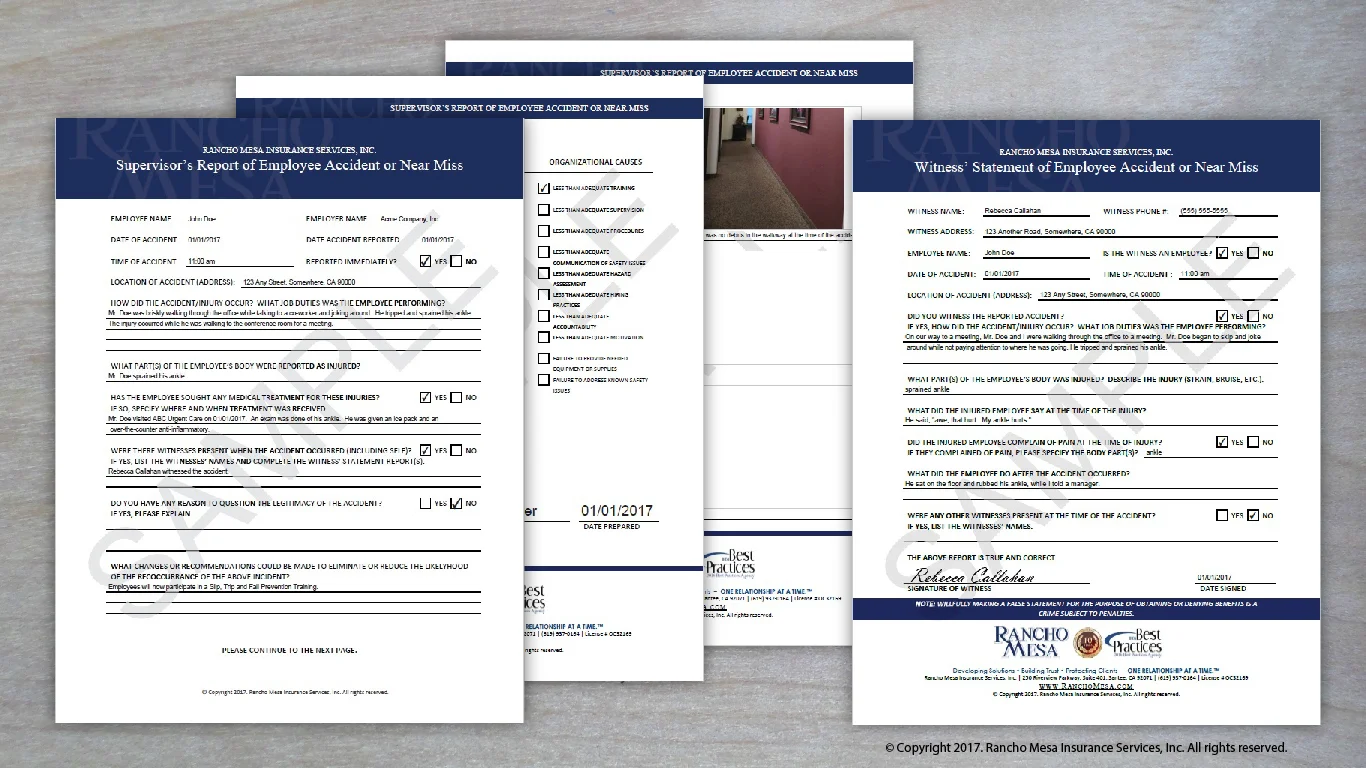

Help Control Your Workers’ Compensation Claim Costs through Accident Investigation

Authors, Dave Garcia, AAI, CRIS, President and CEO, and Drew Garcia, NALP Program Director from Rancho Mesa Insurance Services, Inc.

When a workers’ compensation claims occurs, in order to both control the costs of the claim and look for preventive measures to reduce or eliminate similar claims from reoccurring, it is vital that a thorough accident investigation report is completed.

Authors, Dave Garcia, AAI, CRIS, President and CEO, and Drew Garcia, NALP Program Director from Rancho Mesa Insurance Services, Inc.

When a workers’ compensation claims occurs, in order to both control the costs of the claim and look for preventive measures to reduce or eliminate similar claims from reoccurring, it is vital that a thorough accident investigation report is completed. The accident investigation report should be completed at the time of the accident, by the supervisor overseeing the injured employee, and contain the following information:

- Employee name, date, time and location of the accident,

- A description of how the injury occurred and the job duties the employee was performing when they were injured,

- The employee’s body part(s) that were reported as injured,

- If witnesses were present when the accident occurred, document their names and statements using the Witness’ Statement of Employee Accident or Near Miss Report,

- Pictures of the injury and accident area,

- Recommendations or changes that could be made to eliminate or reduce the potential for a similar claim in the future.

The goals of this process are:

- To have a timely and accurate record of the accident or incident that allows the claim to be reported to the insurance carrier in a timely manner.

- To help you to reduce the chance of fraudulent claims through documentation, pictures and witness statements.

- To analyze the root cause of the accident or near miss and implement the needed recommendations to reduce or eliminate the likelihood of future claims.

As a 10-time National Best Practices Agency, Rancho Mesa Insurance Services, Inc. understands the importance of implementing the highest standards of Risk Management practices for our clients. So, as part of our RM365 Advantage™ program, we have developed our own proprietary Employee Accident Report and Witness Statement to assist our clients with documentation of their accidents or near misses.

How to Prevent Back Injuries in the Landscape Industry

Author, Drew Garcia, with Rancho Mesa Insurance Services, is the program director for NALP’s Worker’s Compensation Program.

According to the Workers Compensation Insurance Rating Bureau (WCIRB), in the last 5 years, over a quarter of a billion dollars in back injury claims, on behalf of the landscape industry, have been paid out by carriers in California. The back claim is by far the most costly injury at $22,000 over the last five years and the second highest in terms of frequency (behind hand, wrist and finger injuries), and the leading claim resulting in an employee's time away from work.

Author, Drew Garcia, with Rancho Mesa Insurance Services, is the program director for NALP’s Worker’s Compensation Program.

According to the Workers Compensation Insurance Rating Bureau (WCIRB), in the last 5 years, over a quarter of a billion dollars in back injury claims, on behalf of the landscape industry, have been paid out by carriers in California. The back claim is by far the most costly injury at $22,000 over the last five years and the second highest in terms of frequency (behind hand, wrist and finger injuries), and the leading claim resulting in an employee's time away from work.

Consider

- Back claims are most costly.

- They are the second most frequent claim reported.

- They are the leading claim resulting in an employee losing time away from work.

Reflect

- Has your company had a back injury in the past?

- What are you doing to protect the backs of your employees?

- Would it be worth your time to consider ways to mitigate this exposure?

Solution

Implementing a pre-work stretch, when done properly, is a quick and effective solution to reduce the likelihood of back injuries. The following stretch program was designed to stretch the back with Professional Landscapers in mind. The program can be executed in minimal time, at any location (yard or on-site) and will not only help employees warm up for the day, but also strengthen their back to help maintain a healthy career.

Benefits

By implementing a stretch you are:

- Showing your employees that you care about their health and have explored an option to help keep them safe.

- Differentiating your companies risk profile against the industry to help enforce aggressive underwriting.

- Looking for a way to improve employee productivity while potentially decreasing insurance cost directly related to claims.