Industry News

Important Reminder for Janitorial Business Owners: Property Service Worker Protection Act

Author, Jeremy Hoolihan, Account Executive, Construction Group, Rancho Mesa Insurance Services, Inc.

A few of my janitorial clients have recently asked for information on the Property Service Worker Protection Act (AB 1978) and its requirements. Below is a description of the law and instructions on registering. As a reminder, the deadline for all janitorial service providers to register for the Property Service Worker Protection Act was October 1, 2018. If you have not yet registered, I would recommend doing so, as soon as possible.

Author, Jeremy Hoolihan, Account Executive, Construction Group, Rancho Mesa Insurance Services, Inc.

A few of my janitorial clients have recently asked for information on the Property Service Worker Protection Act (AB 1978) and its requirements. Below is a description of the law and instructions on registering. As a reminder, the deadline for all janitorial service providers to register for the Property Service Worker Protection Act was October 1, 2018. If you have not yet registered, I would recommend doing so, as soon as possible.

AB 1978 is a law to protect janitors against wage theft and sexual harassment. The law is designed to move the janitorial industry into a modern and transparent industry. There are three main legal mechanisms: record keeping, registration with the Labor Commissioner’s Office, and sexual harassment prevention training.

Recordkeeping

Every employer must keep the following accurate records for three years, showing all of the following:

The names and addresses of all employees who perform janitorial or cleaning services.

The hours worked daily by each employee, including the start and stop times of each work period.

The wage and hourly rate paid each payroll period.

The age of all minor employees.

Any other conditions of employment.

Registration

Every employer who provides janitorial services with a least one employee and one janitor must register with the Labor Commission. An “employer” is broadly defined as any person or entity that employs at least one employee and one or more covered workers and that enters into contracts, subcontracts, or franchise arrangements to provide janitorial services must register yearly with the Labor Commissioner’s office.

To register, an employer must pay a $500 nonrefundable application fee. The registration is valid for one year and must be renewed annually by the month and day of the original registration’s issuance. The renewal fee is also $500. A janitorial employer who fails to register is subject to a civil fine of $100 for each calendar day that the employer is unregistered, not to exceed $10,000.

The documents required to register include:

Fictitious Business Name Statement(s) (doing business as (DBA) for all business name(s) you use or intend to use.

State Employer Identification Number (SEIN) or application for it.

Federal Employer Identification Number (FEIN) or application for it.

Articles of Incorporation, if you are a corporation.

Articles of Organization, if you are a limited liability company (LLC).

Certificate of Limited Partnership, if you are a limited partnership.

Secretary of State Statement of Information, if you are a corporation or LLC.

Proof of workers’ compensation coverage via one of the following:

A valid workers’ compensation insurance certificate which must include the complete and correct name of the legal entity that is the insured employer, including fictitious business names and the complete and correct address for each location.

Certificate of authority to self-insure.

If contracting with an employee leasing company, a current workers’ compensation insurance certificate that is provided to you by the employee leasing company.

Sexual Harassment Prevention Training

The Property Service Workers Protection Act requires janitorial services employers to provide training in the prevention of sexual violence and harassment at least once every two years.

Until the training requirements are established pursuant to Labor Code section 1429.5, employers may meet this obligation by giving employees the Department of Fair Employment and Housing pamphlet DFEH–185, “Sexual Harassment,” in English or Spanish, as appropriate.

Rancho Mesa clients have access to discounted Sexual Harassment Prevention training online in both English and Spanish through the Risk Management Center. Contact Alyssa Burley at (619) 438-6869 for more information.

For more information about the Property Service Workers Protection Act, visit the Department of Industrial Relations website.

How Warranty Periods Can Impact Bonding

Author, Andy Roberts, Account Executive, Surety, Rancho Mesa Insurance Services, Inc.

When we review contracts that require bonding, one area that we need to understand is the warranty obligation. I would expect that over 90% of the contracts that we review for our contractor clients contain a standard one-year warranty term. Since Performance & Payment Bonds respond to the contract, the surety company is also on the hook for this one-year obligation. Premium rates for bonding already include the cost for this one-year warranty in the cost of the performance & payment bond.

Author, Andy Roberts, Account Executive, Surety, Rancho Mesa Insurance Services, Inc.

When we review contracts that require bonding, one area that we need to understand is the warranty obligation. I would expect that over 90% of the contracts that we review for our contractor clients contain a standard one-year warranty term. Since Performance & Payment Bonds respond to the contract, the surety company is also on the hook for this one-year obligation. Premium rates for bonding already include the cost for this one-year warranty in the cost of the performance & payment bond.

What if the warranty period exceeds 12 months?

Depending on the warranty wording of the contract, both the contractor and the surety company can be liable for multiple years of warranty obligation. Anytime that the warranty is going to exceed one year, the surety will charge additional rate for each extra year, which increases the cost of the bond, thereby increasing costs for the principle and ultimately the obligee or owner. Second, and most importantly, increased warranty periods could make it more difficult for a contractor to qualify for a bond for that specific job. The longer the warranty period that the bond will be covering, the longer the surety has to try and project how a contractor or company will be doing at that time. Since they have no real way of doing this, it increases their liability for that particular job and could ultimately lead to a declination for the bond.

One option to consider - for a warranty period of longer than one year (but not specifically stated if the bond will respond to the longer warranty period), the contractor should ask for clarification from the obligee for a couple of different reasons. The owner may confirm that the bond does not have to cover the warranty after the initial one-year period. This will make it easier for the contractor to obtain the bond, because the surety will not be required to respond to a warranty claim several years after a job has been completed. It should be noted that this does not mean the contractor is not bound by the full warranty length stated in the contract.

If your company is interested in working on jobs that require bonding, or you are a contractor with an established surety program but have questions about warranty periods, please contact me at Rancho Mesa Insurance Services 619-937-0164 as I can assist with any questions you may have.

Distracted Driving, Not Just an Automobile Insurance Issue, Bad News for Workers Compensation Too

Author, David J Garcia, A.A.I, CRIS, President, Rancho Mesa Insurance Services, Inc.

I’ve written at length on the negative effects distracted driving is having on the automobile insurance industry and its impact on the rise in accidents, claim costs, and increases to your automobile premiums. But, have you considered its effects on your Experience Modification Rate (EMR) and ultimately workers’ compensation cost?

Author, David J Garcia, A.A.I, CRIS, President, Rancho Mesa Insurance Services, Inc.

I’ve written at length on the negative effects distracted driving is having on the automobile insurance industry and its impact on the rise in accidents, claim costs, and increases to your automobile premiums. But, have you considered its effects on your Experience Modification Rate (EMR) and ultimately workers’ compensation cost?

When one of your employees is injured in an automobile accident while working on your behalf, Arising out of Employment (AOE) / Course of Employment(COE) their sustained injury will be covered by your workers’ compensation policy, regardless of fault.

“Regardless of fault?!”

When a third party is deemed at fault and the injuries to your employee(s) have been settled, your workers’ compensation insurance carrier may “subrogate” their costs to the carrier representing the at fault driver. Now, here is the realty – studies have shown that 14.7% (4.1 million) of all California drivers are uninsured, while another large percentage of drivers hold the California minimum limits of $15,000/$30,000. What this means is that even if subrogation is a possibility, the likelihood of a “full” recovery is not probable. Thus, all the costs of the injury to your employee(s) will likely be the sole responsibility of your workers’ compensation carrier and this claim cost negatively affects your EMR and loss ratios for years to come.

What can you do?

You can implement a strong fleet safety program that includes a policy pertaining to distracted driving. When your employee is involved in a motor vehicle accident, adherence to your company’s accident investigation protocol is crucial. Documentation will prove pivotal for your carrier if subrogation becomes a possibility.

For our clients, through RM365 Advantage, we have a number of resources: fleet safety programs that can be customized, fleet safety training topics, fillable and printable accident investigation forms, archived fleet safety workshop videos, and more, in both English and Spanish. You can access this through our RM365 Advantage Risk Management Center or contact our Client Services Coordinator Alyssa Burley at aburley@ranchomesa.com.

If you are not a current client of Rancho Mesa, we encourage you to reach out to your broker for assistance or email Alyssa Burley to get additional information or to ask any questions.

Fleet Safety: Four Steps to Effective-Driver Selection

Author, Sam Clayton, Vice President Construction Group, Rancho Mesa Insurance Services, Inc.

Driver selection guidelines are one of the most important things a company can implement to prevent vehicle accidents. A company should manage a written Motor Vehicle Records (MVR’s) program to assure that they are selecting the right employees to drive for the company and annually qualify each driver for desirable driving records. The following are some “best practices” guidelines that will help businesses implement and improve the driver selection process.

Author, Sam Clayton, Vice President Construction Group, Rancho Mesa Insurance Services, Inc.

Driver selection guidelines are one of the most important things a company can implement to prevent vehicle accidents. A company should manage a written Motor Vehicle Records (MVR’s) program to assure that they are selecting the right employees to drive for the company and annually qualify each driver for desirable driving records. The following are some “best practices” guidelines that will help businesses implement and improve the driver selection process.

Step 1: Determine who drives for the company.

The first thing a business must do to control driver selections is knowing who is driving on behalf of the company. Most companies have drivers that fall into several categories:

Non-employees operating company vehicles

Drivers of vehicles owned or leased by the company

Drivers with a Commercial Drivers License (CDL)

Employees driving their own vehicle for company business

Step 2: Establish specific requirements depending on whose is driving.

For all employees, regardless if they are operating a company owned or leased vehicle, the company must:

Verify the person has a valid Driver License.

Determine that the license is appropriate for the type of vehicle they will be operating.

Request a copy of their Motor Vehicle Record (MVR) and compare it to the acceptable criteria before they drive for the company, and again on an annual basis.

For drivers of vehicles owned or leased by the company, it is wise to ask for a:

Completed written application that includes a section that lists all driving violations and/or accidents within the last 3 years.

Substance abuse test (optional).

For drivers with a Commercial Driver License:

Conduct a Department of Transportation (DOT) physical examination.

Create a driver qualification file for each driver that complies with DOT.

Conduct a drug test for each driver, following DOT regulations (pre-hire, random, post-accident and suspension).

For employees using their own vehicles for company business:

Require proof of insurance.

Establish minimum personal limits of insurance. Rancho Mesa recommends a minimum of $100,000/$300,000/$100,000.

Step 3: Establish MVR Qualification Process

Managing the driver selection and ongoing qualification process is the employer’s responsibility. There is a broad range of driving violations that can be classified into two major categories “A” and “B.”

Category “A” would include driving under the influence of drugs, refusing to take a substance test, reckless/careless driving, speeding in excess of 14mph over the posted speed limit, texting, hit and run, speeding in a school zone, racing, driving with a suspended or revoked license, vehicular assault etc.

Category “B” would include, speeding 1-14 mph over posted speed limit, improper lane change, failure to yield, failure to obey traffic signal or sign, accidents, having a license suspended in the past for moving violations, etc.

Best practices for MVR qualifications include:

Anyone with a type “A” driving violation in the last five years is undesirable for a driving position.

Anyone with three or more type “B” violations, or two or more at fault accidents in a three-year period, is undesirable for a driving position.

Anyone with two type “B” moving violations, or one driving accident in the last three-year period, should be put on warning and MVR’s reviewed semi-annually.

In addition to the initial MVR check upon hire, all employees who routinely drive their personal vehicle on company business should have their MVR screened at least once every 12 months to ensure their driving record remains acceptable.

Step 4. Enroll all employees in the DMV Pull Notice Program.

For a nominal annual fee, employers can enroll in the Department of Motor Vehicles' Pull Notice Program. This service provides employers with a notice of any moving violations within 24 hours. So, an employer will know right away if one of their drivers' records has changed. Not participating in the program makes the company vulnerable to going months with an unqualified driver before an annual MVR review is completed.

Following these best practices for effective driver selection takes the guest-work out of determining who should drive for a company. Following these four steps can help ensure the company has qualified drivers at all times.

For questions about driver selection, contact Rancho Mesa Insurance Services, Inc. at (619) 937-0164.

Focus on preventing Back Injuries: Introducing Rancho Mesa’s A.B.L.E Lift Protocol and the “Field” Mobility & Stretch Program

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services.

Physical work is demanding on our bodies. As the employer, what are you doing to help your employees prepare for the day’s work? Collectively, the most severe injuries come from the lower back by way of strain or sprain as a result of lifting. It’s not always the heavier objects causing the injuries. In many cases, early morning “light” lifts or movements can quickly cause a strain or sprain.

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services.

Mobility & Stretch Program and ABLE Lift Protocol flyers.

Physical work is demanding on our bodies. As the employer, what are you doing to help your employees prepare for the day’s work? Collectively, the most severe injuries come from the lower back by way of strain or sprain as a result of lifting. It’s not always the heavier objects causing the injuries. In many cases, early morning “light” lifts or movements can quickly cause a strain or sprain. Eliminating lifting exposures is the ultimate solution to limiting back strains; however, it is not always possible. Interactively training your employees to accurately lift material with proper technique is a preventive approach you can implement today to limit your businesses lifting exposure.

Following the success of our “Truck” Mobility and Stretch Program, Rancho Mesa is excited to announce, in conjunction with Collin Dawson CPT., A.B.L.E. “Lift” Protocol to help physically train your employees to execute proper lift decision making and establish the correct physical eliminates it takes to perform a lift. Not all lifts are the same, each one contains different variables, but the same simple body positioning and lift techniques are relevant no matter the exposure.

Our “Truck” Mobility and Stretch Program was highly received and ultimately implemented by many of our clients. Over the past nine months we have worked to address the need for a Mobility and Stretch Program to be lower back specific, but with the ability to perform the exercises without the support of a truck or wall.

We knew the Mobility and Stretch Program would be beneficial. We were surprised to see the amount of clients willing to incorporate this program and ultimately are very pleased with the results, almost one year in. We challenged Collin to create another program that could be performed in a group setting without sacrificing the main purpose of the routine, which is to flex and strengthen the core muscles surrounding the back while providing total body activation. Our “Field” Mobility and Stretch Program does just that, but also provides some opportunity for participants to slowly begin to establish a better center of balance and body awareness, which can be practically applied to the work day and life. We hope this program will be just as well received.

Register for October 25, 2018 webinar where we will detail A.B.L.E. Lift and the recently developed “Field” Mobility and Stretch Program. Only those who attend the webinar will receive the following:

A PDF Mobility and Stretch Program branded to your company (upon request, 10-15 business days to process) “Truck” and “Field” Series

PDF version of A.B.L.E. Lift (8.5x11 and Poster Size)

Recognition on Rancho Mesa website for your participation in the workshop

30-minute complimentary phone assessment with Collin Dawson about these programs and further implementation strategies.

And remember, “Only lift if you are A.B.L.E.”!

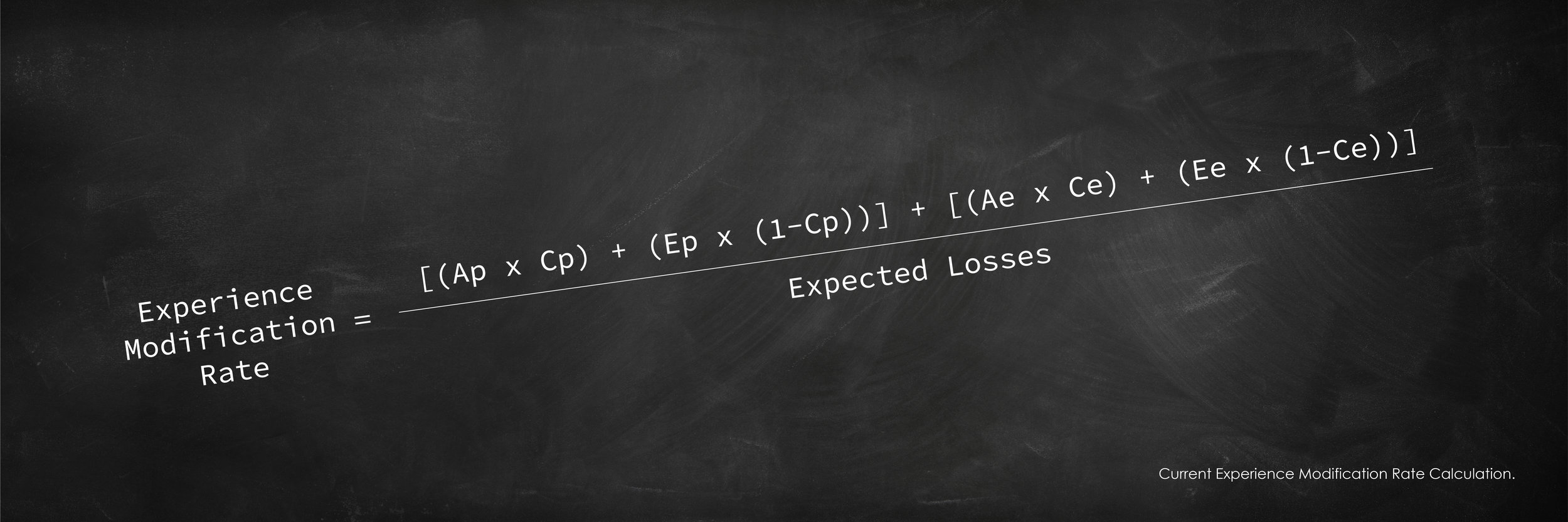

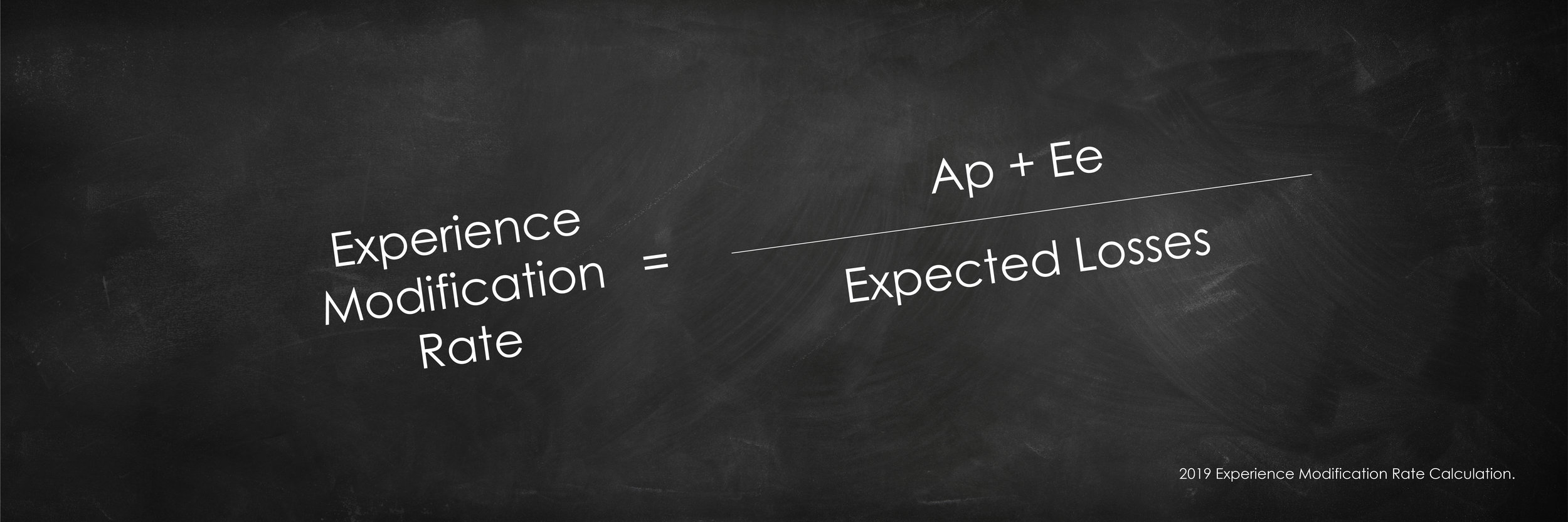

Changes in the 2019 Experience Modification Formula – Are You Ready? (Part 2)

Author, David J. Garcia, A.A.I, CRIS, President, Rancho Mesa Insurance Services, Inc.

As we approach 2019, there will be several changes in the experience modification formula that directly affects the calculation of an employer's 2019 Experience Modification Rate (EMR).

Part 1 of this article describes the Primary Threshold and Expected Loss Rate. Read Part 1 of this article. Part 2 provides an overview of the changes to the EMR calculation.

Author, David J. Garcia, A.A.I, CRIS, President, Rancho Mesa Insurance Services, Inc.

As we approach 2019, there will be several changes in the experience modification formula that directly affects the calculation of an employer's 2019 Experience Modification Rate (EMR).

Part 1 of this article describes the Primary Threshold and Expected Loss Rate. Read Part 1 of this article. Part 2 provides an overview of the changes to the EMR calculation.

The Simplified Formula

Individual claim cost (i.e., both paid and reserved) will go into the calculation up to the primary threshold limit are considered the actual primary losses. Any claim cost that exceeds your primary threshold is considered the actual excess loss. In past experience mod formulas, the actual excess loss was used in the factoring of your EMR; in 2019, it will have no effect. However, under the new calculation, the industry expected excess losses will be considered in the 2019 simplified formula.

Actual Primary Losses + Expected Excess Losses / Expected Losses

The expected excess losses are calculated by multiplying your class code’s payroll per $100 by the expected loss rate for that same class code. This number is then discounted by the “D Ratio” to determine expected primary losses and expected excess losses. There are 90 different D-Ratios for each classification based on the primary threshold. The D-Ratio is different for each classification and is determined by the severity of injuries that occur within that particular class code.

The first $250 of all claims will no longer be used in the calculation of your EMR.

This is a major change and one that was initiated in part to encourage all employers to report all claims, including those deemed first aid, without having a negative impact on the companys’ EMR. This change will affect all claims within the 2019 calculation; so yes, it will include years previously completed and reported. This will have a positive impact on EMRs in that claim dollars will be removed from the EMR calculation.

Confused – Want more details?

Help is on the way. We are going to hold a statewide webinar on Thursday, October 4th at 9:00am in order to dig deeper into this subject and answer specific questions. You may register for the webinar by contacting Alyssa Burley at (619) 438-6869 or aburley@ranchomesa.com.

Contractor Strategies to Maximize Your Bank Line of Credit

Author, Matt Gaynor, Director of Surety, Rancho Mesa Insurance Services, Inc.

Some of my most successful bond clients opened their construction business with a good amount of working experience on their resume, but only a minimal amount of cash and capital. Unfortunately, bond companies like to see a strong amount of cash and capital. Therefore, my goal, as their bond agent, is to work with what they have at the present time to explain why they are a “good risk” now for bid, performance, and payment bonds - along with ideas on how to overcome the initial cash and capital constraints.

Author, Matt Gaynor, Director of Surety, Rancho Mesa Insurance Services, Inc.

Some of my most successful bond clients opened their construction business with a good amount of working experience on their resume, but only a minimal amount of cash and capital. Unfortunately, bond companies like to see a strong amount of cash and capital. Therefore, my goal, as their bond agent, is to work with what they have at the present time to explain why they are a “good risk” now for bid, performance, and payment bonds - along with ideas on how to overcome the initial cash and capital constraints.

As a contractor grows and is looking at larger single and aggregate bond programs, I make it a point to work with the contractor on upgrading their financial presentation along with the goal to qualify for a Bank Line of Credit. It can sometimes be difficult to qualify for that “first” bank line of credit.

We want to help! On Friday, September, 28th, we will be inviting a local bank professional to cover "Contractor Strategies to Maximize their Bank Line of Credit." Our goal is to answer some of the following questions to prepare the contractor for a favorable submission process with the banker:

a) What is the typical information needed from the Contractor to apply for a Bank Line?

b) How do I determine what size Line of Credit I should ask for?

c) What are the “key” underwriting areas you will concentrate on?

d) How long after we provide you the information should we expect an answer?

e) To qualify for a line of credit – do we need to move our checking account to your Bank?

The seminar will allow us to pull back the curtain with the banker to make this process as seamless and painless as possible. The seminar will provide the contractor an opportunity to ask the questions you might have avoided because you assumed you did not qualify.

If interested, please register online or contact Rancho Mesa Insurance at (619) 937-0164.

Changes in the 2019 Experience Modification Formula – Are You Ready? (Part 1)

Author, David J. Garcia, A.A.I, CRIS, President, Rancho Mesa Insurance Services, Inc.

As we approach 2019, there will be several changes in the experience modification formula that directly affects the calculation of an employer's 2019 Experience Modification Rate (EMR). Sadly, most businesses are both unaware and unprepared.

Author, David J. Garcia, A.A.I, CRIS, President, Rancho Mesa Insurance Services, Inc.

As we approach 2019, there will be several changes in the experience modification formula that directly affects the calculation of an employer's 2019 Experience Modification Rate (EMR). Sadly, most businesses are both unaware and unprepared.

Before we breakdown the changes to the 2019 EMR formula, we must first have a strong understanding of the two critical components that directly affect the outcome of the EMR. This article will be broken out into 2 parts. Part 1 will describe the Primary Threshold and Expected Loss Rate. In Part 2, I will provide an overview of the changes to the EMR calculation.

The single most important number to my EMR is not my final rating?

Primary Threshold

Rancho Mesa has long taken a stance on the importance of a business owner knowing their primary threshold as it relates to the EMR. Proactive business owners should monitor their primary threshold annually as it is subject to change due to payroll fluctuations, operations, and the annual regulatory filing of the expected loss rate. In general terms, the more payroll associated with your governing class (the class code with the preponderance of your payroll) the higher your primary threshold will be. The primary threshold is unique to every business. The 2019 EMR formula is heavily weighted by the company's actual primary losses, the claim cost (both paid and reserved) that goes into the calculation up the primary threshold amount. Controlling claim cost and knowing your company's primary threshold is the first step to understanding the EMR.

Expected Loss Rates

The expected loss rate is the factor used to anticipate a class code's claim cost per $100 for the experience rating period. The expected loss rate (ELR) is not to be confused with the pure premium rate (PPR). The ELR differs from the PPR in that the ELR simply measures the basic claim cost for a class code without including loss adjustment expense, excess loss load (capped at $175,000 for X-MOD purposes), and loss development. The PPR includes all of the mentioned above factors and is the rate for which a carrier can expect to pay all of the cost associated with claims in a specific industry. The PPR does not account for the carrier’s overhead, profit, tax, and commissions.

The ELR changes, annually. It’s important to monitor the change; if your expected loss rates go down (from our analysis this is the direction most are going) and if nothing else changes, your EMR will go up. Why is this? Again, without going too deep, in simple terms, your EMR is a ratio of actual losses to expected losses. If your expected losses go down, but your actual losses remain the same, then your EMR will go up.

To illustrate this, consider the following. Actual losses are $25,000 and your expected losses are $25,000 your EMR would be 100. Now, if your actual losses stay the same at $25,000, but your expected losses drop to $20,000, your EMR would now be 125%. (There are other factors that would go into the actual calculation, so your actual EMR would be different – this was just to illustrate the expected losses impact to the EMR.)

In Part 2 of this article, will cover the actual changes to the EMR calculation.

For more information about the EMR, contact Rancho Mesa Insurance Services at (619) 937-0164.

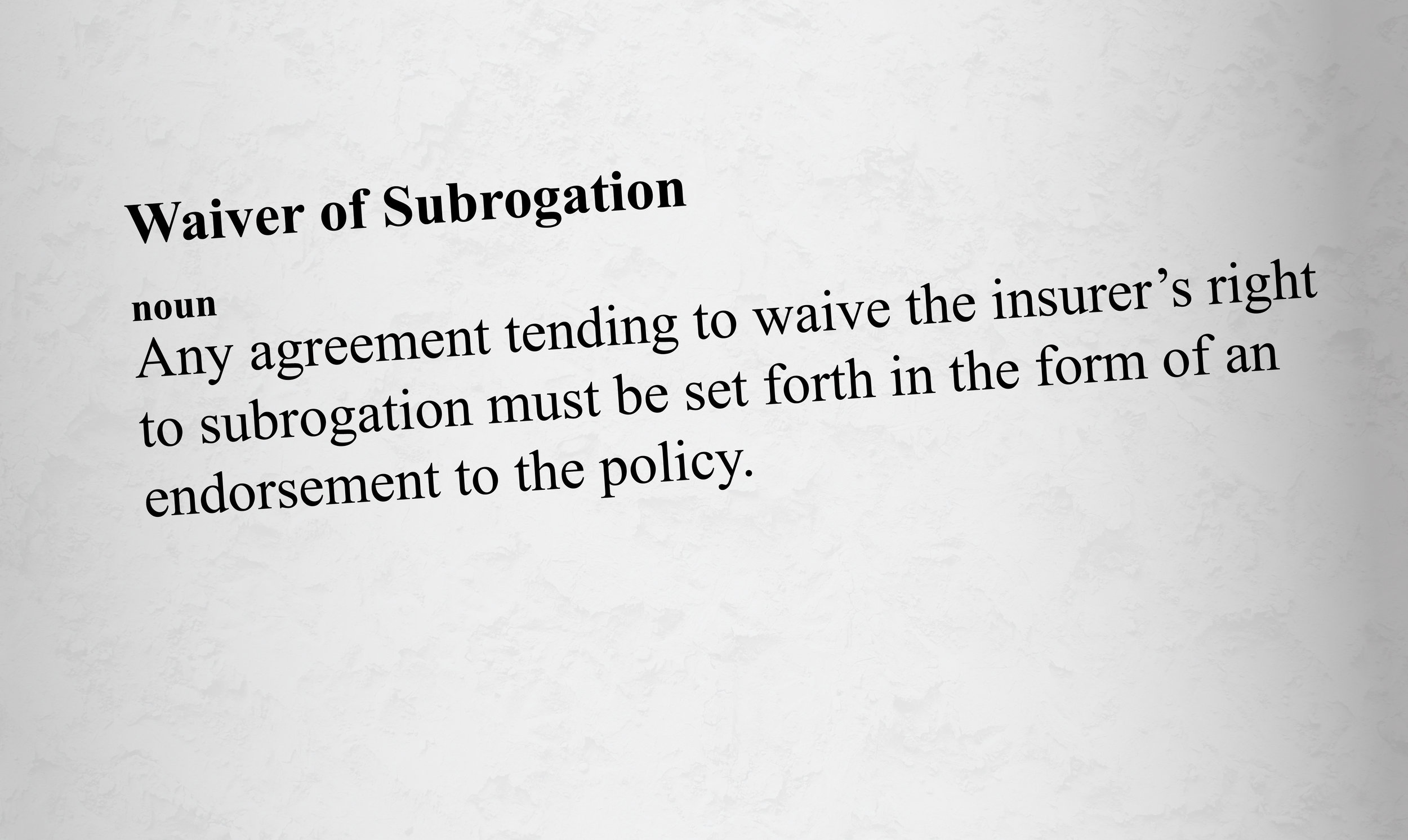

Understanding Waivers of Subrogation for Contractors

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

In an era where general contractors commonly require a Waiver of Subrogation from its sub-contractors before they are allowed to step foot on the jobsite, it is important to understand how a Waiver of Subrogation functions. Most companies simply tell their agent they need the waiver added to their contract, but what does this mean? How does it affect the policy?

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

In an era where general contractors commonly require a Waiver of Subrogation from its sub-contractors before they are allowed to step foot on the jobsite, it is important to understand how a Waiver of Subrogation functions. Most companies simply tell their agent they need the waiver added to their policy, but what does this mean? How does it affect the policy?

Subrogration is "the legal process by which an insurance company, after paying for a loss, seeks to recover all or a portion of the loss from another party who is legally wholly or partially liable for that loss," according to the Workers' Compensation Insurance Rating Bureau of California (WCIRB). So, a Waiver of Subrogration prevents your insurance carrier from recovering funds paid on a claim from the named party requesting the waiver.

When subrogating, three things must be established:

1) The defendant was negligent (or that a product was defective),

2) Negligence proximately caused the damages for which the carrier paid, and

3) The amount and nature of the damages.

If you cannot establish any one of these three, there will be no subrogation.

Subrogation is used throughout various lines of insurance. It is very common in dealing with auto insurance claims. If you are in an accident and the other driver is deemed to be at fault, your insurance company will respond first by paying to have your vehicle fixed. Then, the carrier will collect from the at fault driver’s insurance company to recover the amount they had to pay to fix your car. The insured’s carrier jumps on the claim immediately so that the insured will not have to wait for the claim to be disputed and resolved before their car is repaired. Claims are handled the same for every line of insurance, unless there is a Waiver of Subrogation in place.

When a sub-contractor is hired and has signed a Waiver of Subrogation for the project owner or general contractor, they are essentially waiving their carrier's ability to recover the money that was paid out on a claim that was caused by a third party's negligence. Waivers of subrogation often come in two formats. Either, the waiver specifically names an entity that the carrier waives its’ right to subrogate against, or a Blanket Waiver of Subrogation. If a Blanket Waiver of Subrogation is provided, the carrier must obtain permission from the named insured to subrogate against a third party.

When adding a Blanket Waiver of Subrogation to a policy, there is an additional fee to offset the carrier’s ability to reclaim money from any losses that were caused by a third party's negligence. These fees can change from carrier to carrier and it is a good move to review each policy to know exactly what you are paying for waivers. Adding a blanket waiver of insurance does not increase coverage or limits, it simply absolves an owner/general contractor of their liability.

With Waivers of Subrogation becoming more prevalent, it is easy to see how important it is as a business owner to know exactly what is covered and what you are waiving.

If you have any questions or would like to understand subrogation further, please contact Rancho Mesa at (619) 937-0164.

Differentiating Solar Industry Class Codes

Author, Kevin Howard, Account Executive, Rancho Mesa Insurance Services, Inc.

Research conducted by the Solar Energy Industry Association (SEIA) shows that California benefits from roughly 3,000 solar contractors conducting business in the state. Panels are being installed at a rapid rate. In fact, statistics show that as of January 2018, over 5 million California homes have “gone solar” and that number continues to grow. There are other benefits to using solar panels to harvest energy besides just generating electricity. They can also be used to heat water in pools, spas, storage tanks and other plumbing systems using hot water solar panels.

Author, Kevin Howard, Account Executive, Rancho Mesa Insurance Services, Inc.

Research conducted by the Solar Energy Industry Association (SEIA) shows that California benefits from roughly 3,000 solar contractors conducting business in the state. Panels are being installed at a rapid rate. In fact, statistics show that as of January 2018, over 5 million California homes have “gone solar” and that number continues to grow. Not only are solar panels used to generating electricity, they can also be used to heat water in pools, spas, storage tanks and other plumbing systems using hot water solar panels.

With solar installation of all kinds becoming more prevalent throughout California, contractors must understand which workers' compensation classification is most applicable for their specialty.

California’s Workers' Compensation Insurance Rating Bureau (WCIRB) breaks down solar installation into two categories: (1) Hot water solar collection panel install, service and repair, and (2) Photovoltaic (PV) solar panel install, service and repair.

Hot Water Solar Collection Panel Install, Service and Repair

Hot water solar collection panels absorb solar energy to heat water or to transfer fluid that circulates through panels. This hot water is then routed through pipes to pools, spas, storage tanks or hydraulic heating systems. The installation, service or repair of solar water panels is assigned to workers' compensation class code 5183/5187 for plumbing.

PV Solar Panel Install, Service, and Repair

This classification applies to the outside installation, service or repair of electrical machinery or auxiliary apparatus, including but not limited to automated security gates, transformers, generators, control panels, temporary power poles at construction sites, industrial fans or blowers, photovoltaic solar panels, wind powered generators and industrial x-ray machines. Contractors who are installing, servicing or repairing PV solar panels will be assigned to the class code 3724(2) in electrical machinery or auxiliary apparatus.

The workers compensation base rates for each of these two class codes can vary widely from one carrier to another. Solar installation exposures, a detailed description of operations, and appropriate safety measures utilized must be clarified with your insurance broker so that your firm is properly placed in the appropriate code. The difference can often represent significant savings.

Rancho Mesa Insurance Services, Inc. has expertise in the solar contracting arena, representing clients that cross into both categories. Consider Rancho Mesa for a policy review and audit in advance of your next insurance renewal.

Three Reasons to Read Subcontractor Warranty Endorsements

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

Contractors General Liability Policies provide coverage for bodily injury and property damage for which the Named Insured is legally liable. This legal liability can result from the company’s direct operations or from other subcontractors hired by the Named Insured.

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

Contractors General Liability Policies provide coverage for bodily injury and property damage for which the named insured is legally liable. This legal liability can result from the company’s direct operations or from other subcontractors hired by the named insured.

Many general liability carriers will include some form of subcontractor warranty endorsement which establishes minimum requirements for subcontractors relative to insurance and other risk management benchmarks. At a minimum, these forms require written indemnification in favor of the named insured, certificates of insurance with additional insured wording, and specific insurance limits required by subcontractors.

These endorsements can vary widely from carrier to carrier; so, contractors may be faced with serious consequences in the event that requirements are not met. Below are three types of penalties policyholders may encounter:

- Coverage is DENIED relative to any loss resulting from the work of the subcontractors.

- Coverage is not altered, but a higher deductible or retained limit applies to any loss resulting from the work of the subcontractor. For example, should you fail to comply with the warranty, the deductible on the policy is amended from $5K to $25K.

- Coverage is not altered, but failure to comply will result in an additional premium charged at the final audit.

It is critical to have a strong contractual written transfer program in place with proper certificates of insurance from your subcontractors, regardless of the contract amount. Lean on your broker to interpret these endorsements and help negotiate the most favorable terms as you head into your renewal. Understanding these nuances can be the difference between a covered loss and an unexpected large capital expense.

For more information about subcontractor warranty endorsements, contact Rancho Mesa Insurance Services, Inc. at (619) 937-0164.

Six Reasons a Company’s Experience Modification Could be Recalculated

Author, Jeremy Hoolihan, Account Executive, Rancho Mesa Insurance Services, Inc.

Workers’ Compensation costs continue to be one of the most costly expenses for business owners in California. With recent reform, California has maintained steady rate decreases in the workers’ compensation marketplace. Unfortunately California still maintains some of the highest rates in the country, often times two to three times the nations average.

Author, Jeremy Hoolihan, Account Executive, Rancho Mesa Insurance Services, Inc.

Workers’ Compensation costs continue to be one of the most costly expenses for business owners in California. With recent reform, California has maintained steady rate decreases in the workers’ compensation marketplace. Unfortunately, California still maintains some of the highest rates in the country, often times two to three times the nations average.

Controlling insurance costs is vital to staying profitable and often times, staying in business. An important way business owners can control their insurance costs is by controlling their Experience Modification or X-MOD. An X-MOD is a benchmark of an individual employer against others in its industry, based on that employer's historical claim experience. This comparison is expressed as a percentage which is applied to an employer's workers' compensation premium.

The premium impact of a credit X-MOD (less than 1) vs a debit X-MOD (more than 1) can be significant. Business owners budget around their insurance costs. When there are unforeseen changes to their insurance costs it can have a dramatic effect. While it is rare, there are situations when an X-MOD can change in the middle of a policy term. Below are six circumstances when this could happen:

- If a claim that has been used in an X-MOD calculation is subsequently reported as closed mid policy term AND closed for less than 60% of the aggregate of the highest value, then the X-MOD is eligible for recalculation.

- In cases where loss values are included or excluded through mistake other than error of judgement. Basically, this rule takes into consideration the element of human error.

- Where a claim is determined non-compensable. Meaning the injury was determined to be non-work related.

- Where the insurance company has received a subrogation recovery or a portion of the claim cost is declared fraudulent.

- Where a closed death claim has been compromised over the sole issue of applicability of the workers’ compensation laws of California. Basically, if a person passes away at work but it was determined that the person had a pre-existing condition which caused the death, not work itself.

- Where a claim has been determined to be a joint coverage claim. This occurs mainly with cumulative trauma claims where there was no specific incident that caused an injury, but an injury that developed over time (i.e., wear and tear).

If any of the circumstances above have occurred, than a revised reporting shall be filed with the Workers’ Compensation Insurance Rating Bureau (WCIRB) and it shall be used to adjust the current and two immediately preceding experience ratings.

If you would like to discuss this topic in further detail, and learn how Rancho Mesa Insurance can audit your X-MOD worksheet for potential recalculations, please contact us at (619) 937-0164.

Six Proactive Steps to Prevent Heat Illness During a Scorching Summer

Author, Dave Garcia, President, Rancho Mesa Insurance Services, Inc.

The National Weather Service has issued heat warnings for many parts of California starting today, and excessive heat warnings for some other areas. Temperatures are expected to rise to 110ºF in some parts of the Sacramento Valley, for instance. In the desert areas of Imperial and San Diego counties, they will soar as high as 114ºF.

Author, Dave Garcia, President, Rancho Mesa Insurance Services, Inc.

The National Weather Service has issued heat warnings for many parts of California starting today, and excessive heat warnings for some other areas. Temperatures are expected to rise to 110ºF in some parts of the Sacramento Valley, for instance. In the desert areas of Imperial and San Diego counties, they will soar as high as 114ºF.

Recommendation

If you have employees working outdoors, you should have an effective heat illness prevention plan in place and train your workers on it's content. Elements of the plan include:

- Making sure those toiling outside have plenty of fresh, cool water – workers need to drink at least a quart an hour. Just providing it isn’t enough, according to the heat illness prevention standard (General Industry Safety Orders section 3395). You must encourage employees to drink water.

- Providing shade when the temperature reaches 80ºF, or when employees request it.

- If an employee is in danger of developing heat illness, they must be allowed to take a rest in the shade until their symptoms disappear.

- Having emergency procedures, including effective communication with workers in remote areas.

- Designating employees at each work site to call emergency medical services if someone starts to develop heat illness.

- Keeping a close eye on workers who have been on the job for two weeks or less. They may not have the prior training to be aware of the early signs of heat illness.

In order to prepare our clients, Rancho Mesa recently conducted a Heat Illness Prevention Workshop. For those of you who were not able to attend, the training videos are available in the Risk Management Center or via the Workshop Video Request Form.

Should you have any questions or need further assistance, please contact a member of your Rancho Mesa team. Please be safe!!

Independent Contractor Classification Changes Expected to Impact Construction Industry

Author, David J. Garcia, AAI, CRIS, President, Rancho Mesa Insurance Services, Inc.

With the recent ruling by the California Supreme Court concerning how 1099 employees (independent contractors) are defined, the construction industry's approach to utilizing these workers has changed significantly. The Court adopted a new test to determine whether the worker should be classified as an employee or independent contractor. The previous test to determine if a worker was an employee or independent contractor was whether the employer had the right to direct the manner and means by which the worker performed the services.

Author, David J. Garcia, AAI, CRIS, President, Rancho Mesa Insurance Services, Inc.

With the recent ruling by the California Supreme Court concerning how 1099 employees (independent contractors) are defined, the construction industry's approach to utilizing these workers has changed significantly. The Court adopted a new test to determine whether the worker should be classified as an employee or independent contractor. The previous test to determine if a worker was an employee or independent contractor was whether the employer had the right to direct the manner and means by which the worker performed the services. Under the new test, a worker is considered to be an independent contractor only if all three of the following factors are present:

- The worker must be free from the control and direction of the hiring entity in connection with the performance of the work, both under the contract for the performance of the work and in fact;

- The worker must perform work that is outside the usual course of the hiring entities business;

- The worker must be customarily engaged in an independently established trade, occupation, or business of the same nature as that involved in the work performed.

These new factors have major implications for contractors, or any business for that matter, where previously they had classified a worker as an independent contractor and now have to classify them as an employee. This will impact several lines of insurance, but most critically workers' compensation, general liability and employee benefits.

Workers' Compensation

Currently, if an employee is classified as an independent contractor, they would not be subject to any workers' compensation premium nor workers' compensation benefits. If their status should change to employee, they now would be entitled to workers' compensation benefits and would have their payroll accounted for in the employer’s premium. In addition, based on the work being performed, this may change the employer’s risk profile, creating negative underwriting consequences in the workers' compensation carrier marketplace, resulting in coverage not being offered or higher premiums.

General Liability

The impact to general liability insurance is very similar to that of workers' compensation. Additional payroll or sales will need to be accounted for as the employer will become directly responsible for the work being performed without the benefit of any hold harmless agreement or other risk transfer methods. This could potentially change the risk profile of the employer’s operations, which could result in the employer needing to provide additional underwriting information.

Employee Benefits

Since 1099 contract workers are not employees and are considered self-employed, they do not show on the Quarterly Wage and Withholding Report (DE9 and DE9C) to the State of California. Because of this status, they typically cannot enroll in a group health insurance plan. Many workers who are now classified as independent contractors will be considered employees in the eyes of the state and will be eligible for group benefit offerings from their employer.

Employers may need to reevaluate their group size to ensure that they remain compliant with the Affordable Care Act (ACA). Employers with 50 or more full-time employees working a minimum of 30 hours per week, and/or full-time equivalents (FTEs) must offer health insurance that is affordable and provides minimum value to 95% of their full-time employees and their children up to age 26, or be subject to penalties.

While these changes are new and just beginning to take affect, we believe your best strategy moving forward is to consult with your trusted advisors in legal, accounting and risk management. This will have a significant impact to the construction industry throughout California and we intend to take a leadership role in helping those companies with concerns and questions. So, please reach out to our Rancho Mesa Team to help you navigate these changes. Contact Alyssa Burley at aburley@ranchomesa.com for assistance.

Key Steps to Take Before, During, and After an OSHA Inspection

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

An OSHA officer can show up to your facility or worksite for any number of reasons: employee complaints, accidents, programmed inspections, sweeps, follow-up or a drive-by observation. In order to ensure a smooth inspection, we suggest you prepare before OSHA appears at your door. Here are some key steps to take before, during and after an OSHA inspection.

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

An OSHA officer can show up to your facility or worksite for any number of reasons: employee complaints, accidents, programmed inspections, sweeps, follow-up or a drive-by observation. In order to ensure a smooth inspection, we suggest you prepare before OSHA appears at your door. Here are some key steps to take before, during and after an OSHA inspection.

Before the Inspection

Every company should have a formal plan in place detailing what should be done before, during and after an OSHA inspection. This procedure should be site specific and available to all supervisors. Site specific information should include company contacts for the project if OSHA arrives, location of documents like OSHA 300 logs and the Injury and Illness Prevention Program (IIPP).

Upon arrival of the OSHA inspection officer, the company should verify the officer’s credentials and try to determine why they are at the site. Before the opening conference begins, the employer should assign specific individuals to be the note taker and the photographer. It is also extremely important to remind everyone involved to be professional and treat the compliance officer with respect.

During the Inspection

Opening Conference: During the opening conference, you will want to establish the scope of the inspection, the reason for the inspection, and the protocol for any employee interviews or production of documents. If the inspection is triggered by an employee complaint, the employer may request a copy.

Physical Inspection: During the inspection, the OSHA compliance officer will conduct a tour of the worksite or facility in question to inspect for safety hazards. It is likely pictures will be taken by the compliance officer. Instruct your photographer to also take the same pictures and possibly additional pictures from different angels while the note taker should take detailed notes of the findings.

Closing Conference: At the closing conference, the OSHA compliance officer typically will explain any citations, the applicable OSHA standards and potential abatement actions and deadlines. It is important that during this process the company representative takes detailed notes and asks for explanations regarding any violations. If any of the alleged violations have been corrected, you will want to inform the OSHA compliance officer.

After the Inspection

If you are told no citations will be issued, contact the compliance officer and obtain a Notice of No Violation after Inspection (Cal/OSHA 1 AX). If you receive a citation, it is important to take immediate action because a company only has 15 working days after the inspection to notify the Appeals Board, if they choose to appeal the citation. Citations can be issued up to six months after the inspection, so it is important to watch your mail closely during this time.

For a proactive approach to OSHA inspections, contact the Consultation Services Branch for your state (i.e. Cal/OSHA) or Federal OSHA Consultation. They will be able to provide consultative assistance to you through on-site visits, phone support, educational materials and outreach, and partnership programs.

Register for the "How to Survive an OSHA Visit" webinar hosted by KPA on Monday, June 25, 2018 from 11:00 am - 12:00 pm PST to learn about what OSHA looks for during an inspection.

For additional information, please contact Rancho Mesa Insurance Services, Inc. at (619) 937-0164.

How a Bank Line of Credit Can Affect Your Surety Bonding

Author, Andy Roberts, Account Executive, Surety, Rancho Mesa Insurance Services, Inc.

When a surety carrier is evaluating a bonding program for a contractor, they use many different underwriting factors to determine an acceptable amount of bond capacity. They will consider a contractor’s working capital, net worth and work in progress schedules, to name a few. Another important factor that can help increase a contractor's bonding capacity is a bank line of credit.

Author, Andy Roberts, Account Executive, Surety, Rancho Mesa Insurance Services, Inc.

When a surety carrier is evaluating a bonding program for a contractor, they use many different underwriting factors to determine an acceptable amount of bond capacity. They will consider a contractor’s working capital, net worth and work in progress schedules, to name a few. Another important factor that can help increase a contractor's bonding capacity is a bank line of credit.

The construction industry is very unpredictable and unforeseen issues can arise that may interrupt jobs and cash flow. Surety carriers place such a high value on a bank line because it provides access to cash that may be critical to continuing the day to day operations and survival of the contractor's business.

While bank lines are an important factor that underwriters use, the lines should not be depended upon for frequent use. Dependency on a line can be a sign that the contractor may have some deeper financial issues. Contractors should try to have at least 30 consecutive days during the course of the year, where they do not use their bank line at all.

If your company is interested in working on jobs that require bonding, or you are a contractor with an established surety program but interested in ways to increase the programs limits, please contact me or Matt Gaynor at Rancho Mesa Insurance Services 619-937-0164 as we can assist with any questions you may have.

Why Painting Contractors Need Pollution Liability Insurance

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

At first glance, most painting contractors don’t think they need pollution coverage. One might think that if they're not pouring sludge into a lake or toxic gasses into the atmosphere, then it wouldn’t apply to their company. Everyone sees the oil spills and thinks that this is what pollution coverage is for, but how does it apply to your smaller business? How can one event jeopardize your company’s success?

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

At first glance, most painting contractors don’t think they need pollution coverage. One might think that if they're not pouring sludge into a lake or toxic gasses into the atmosphere, then it wouldn’t apply to their company. Everyone sees the oil spills and thinks that this is what pollution coverage is for, but how does it apply to your smaller business? How can one event jeopardize your company’s success?

In reality, pollution coverage is a must have policy for all painting contractors. This is how your business could be at risk.

First, let's determine what is a pollutant. A pollutant is defined as “the discharge, dispersal, release or escape of any solid, liquid, gaseous or thermal irritant or contaminant, including, but not limited to, smoke, vapors, soot, fumes, acids, alkalis, toxic chemicals, medical waste and waste materials into or upon land, or any structure on land, the atmosphere or any watercourse or body of water, including groundwater, provided such conditions are not naturally present in the environment in the amounts or concentrations discovered.” It is shocking how often a painting contractor is exposed to mold, asbestos, bacteria, or paint fumes.

What does Contractors Pollution Liability Insurance (CPL) really cover? CPL is a contractor-based policy, offered on a claims-made or occurrence basis, that provides third-party coverage for bodily injury, property damage, defense, and cleanup as a result of pollution conditions (sudden/accidental and gradual) arising from contracting operations performed by or on behalf of the contractor.

There are countless stories of something unforeseen being the cause of a pollution claim. Here are just a couple examples that could apply to your company.

A contractor had painted a nursing home and was sued by the residents. They alleged that the fumes weren’t ventilated properly. That claim alone was over $200,000.

A painter was removing lead paint from a bridge and some flakes fell into the river below. The damages exceeded $500,000.

A pollution claim could arise from site runoff after it rains, or accidentally drilling into a water pipe in the wall that produces leakage that leads to mold exposure. While transporting paint to a jobsite, the driver could get into an accident and the paint spills out and contaminates a water source adjacent to the road.

Most businesses look at pollution risk as something that doesn’t apply to them. Obviously, they aren’t planning on releasing pollutants like bacteria, mold, or fumes while on a jobsite. But, all it takes is one claim that could cost your company. Investigation costs, medical expenses, lawsuits, cleaning up of the area properly, not to mention how important your reputation is to your success, any one of these factors could be enough to bring your business to an end.

Some contractors believe all third-party problems are covered by their general liability policy; however, most general liability policies will contain a pollution exclusion which doesn’t cover any property damage or bodily injury that comes from the result of a pollution event. Your general liability policy will not cover the cost of clean-up, either. It is easy to see how this could become a costly event, very quickly.

It is very clear to see the dangers that surround your business. Now that you know what they are, protect your business with CPL insurance. Contact me at (619)438-6900 or email me at ccraig@ranchomesa.com with any further questions. Let’s make sure you are properly prepared to protect your company’s future.

CIGA is “Back in Black” - Employers will receive 2% savings on 2019 workers' comp premium

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

For the first time in 20 years, the California Insurance Guarantee Association (CIGA) will not collect its annual assessment. As a result, California employers in the guaranteed cost workers' compensation insurance market will save 2% on their premium in 2019.

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

For the first time in 20 years, the California Insurance Guarantee Association (CIGA) will not collect its annual assessment. As a result, California employers in the guaranteed cost workers' compensation insurance market will save 2% on their premium in 2019.

The CIGA board of directors approved a zero assessment for 2019, as it moved into the black after collecting last year’s 2% assessment on workers' compensation premiums. At one point, CIGA had a workers, compensation deficit of $4 Billion. The 20 years of employer assessments, ranging from 1% to 2.6% of premium, paid off workers' compensation debt and in some years the debt payments on special bonds issued to pay claims from insurance company insolvencies.

Similar to the rest of the Industry, CIGA’s improved fortune results from positive reforms provided in SB 863, as well as the efforts of Department of Industrial Relations Director Christine Baker.

Three Question to Ask Before Enrolling in an OCIP/CCIP or Wrap Program

Author, Daniel Frazee, Executive Vice President, Rancho Mesa Insurance Services, Inc.

Subcontractors in California regularly enroll in OCIP/CCIP or wrap programs. These programs are insurance policies that cover many of the participants in a construction project, including the owner/developer, general contractor and subcontractors. As many contractors learn the hard way, they do not control the program or the coverage terms, leaving the possibility of significant gaps that can impact the contractor in the future.

Author, Daniel Frazee, Executive Vice President, Rancho Mesa Insurance Services, Inc.

Subcontractors in California regularly enroll in OCIP/CCIP or wrap programs. These programs are insurance policies that cover many of the participants in a construction project, including the owner/developer, general contractor and subcontractors. As many contractors learn the hard way, they do not control the program or the coverage terms, leaving the possibility of significant gaps that can impact the contractor in the future.

Prior to enrolling in a wrap insurance program, consider developing a list of key questions to regularly ask the plan sponsor. Before you begin that process, subcontractors need to know what information the plan sponsor is obligated to share about the project. And, that obligation varies greatly, depending on whether the project is public, private, or residential. Additionally, the statutory disclosure requirements are inconsistent in how they appear in the contract and bid documents. The following are a summary of those disclosures.

Residential Project Contract Documents

For residential projects, the contract documents must disclose, if and to the extent known, (Civil Code section 2782.95(a)):

- Policy limits

- Scope of policy coverage

- Policy term

- The basis upon which the deductible or occurrence is triggered by the insurance carrier

- Number of units, if the policy covers more than one work improvement indicated on the application for the insurance policy

- A good faith estimate of the amount of available limits remaining under the policy as of a date indicated in the disclosure obtained from the insurer.

Public and Commercial Project Contract Documents

For public and commercial projects, subcontractors are entitled to even less information, under (Civil Code section 2782.96):

- The policy limits

- Known exclusions

- The length of time the policy is intended to remain in effect.

In both cases above, the information that the plan sponsor is required to provide is far less than subcontractors need to truly make an informed decision on the coverage terms. Knowing now that enrollees have the right to ask for these insurance requirements before bidding the job, we will prioritize three important questions to begin the framework for your due diligence.

What are the Limits of Coverage?

Work inside OCIP/CCIP or wrap programs is commonly excluded on all contractor’s general liability policies. As a result, coverage is found almost entirely within the policy limits in place for the wrap program. That leaves key questions for your team to explore before stepping foot on a jobsite. What are the total costs of construction relative to policy limits? Are there any other projects being covered under the Wrap policy? Are the limits of insurance reinstated after a large loss? Do defense costs reduce the policy limits? While there are certainly more questions inside this vertical, knowing these initial answers and being familiar with what impact they may have on your business are a solid first step in your process.

What is Covered and What is Excluded?

Wrap programs, as many subcontractors know, can provide coverage for both general liability and workers' compensation. In the last few years, Wrap policies have focused more on general liability. Many can also include builder’s risk, professional and/or pollution liability. Each project, and therefore each wrap policy, is very unique. Be prepared to negotiate the removal of certain exclusions that often relate to some, but not all, subcontractors:

- Subsidence (earth movement)

- Professional Liability (also referred to as errors & omissions - typically a separate policy)

- Pollution Liability (typically a separate policy)

- Offsite work

What Deductible or Self-Insured Retention (SIR) is Required?

There are limited protections for wrap participants regarding the amount of self-insured retentions and/or deductibles, particularly with public or commercial projects. Subcontractors must identify, for example, the size of the deductible and whether that contribution is shared or individual. Deductibles within wrap policies can be as high as $25,000 - $50,000 per claim, which can represent significant impacts to a subcontractor’s balance sheet when unprepared.

Whenever you are considering a project that requires you to enroll within a OCIP/CCIP or wrap program, your due diligence in understanding the full scope of the insurance being offered is of the utmost importance. Discuss this in detail with your broker or reach out to one of us in our constructions group to help you navigate your way through the process.

Case Study: First-Time Bonding for Landscape Professional

Author, Matt Gaynor, Director of Surety, Rancho Mesa Insurance Services, Inc.

I recently had the opportunity to work with a new client who is a landscape professional. He wanted to bid on a maintenance project for a local municipality and wasn’t sure if he would qualify for the required performance bond.

Author, Matt Gaynor, Director of Surety, Rancho Mesa Insurance Services, Inc.

I recently had the opportunity to work with a new client who is a landscape professional. He wanted to bid on a maintenance project for a local municipality and wasn’t sure if he would qualify for the required performance bond.

After a brief discussion of how bonding differs from insurance, we decided to collect some basic information to determine if he would “pre-qualify” for the bond before putting together a full submission. The bond company ran the personal credit of the owner and determined that they would support single bonded projects up to $500,000.

After a careful review of the project specifications, the client decided not to bid on the project. We mutually decided he should provide additional information to the bond company in the event he wanted to bid on a larger project that was going to be released in the following month. The information requested by the bond company included:

a.) Completed contractor questionnaire

b.) Two year-end financial statements or tax returns for the company

c.) A personal financial statement for the owner(s)

Based on the additional information provided, we were able to negotiate a $1,000,000 single project / $3,000,000 aggregate bonding program for this particular landscape professional. The client executed the bond company general indemnity agreement and was off and running to bid the larger projects.

Make sure you work with a professional surety agent who can help assist with the bonding process if you are considering bidding on public works projects. It can save you a lot of time and effort.

Contact Rancho Mesa at (619) 937-0165 if you have any bonding questions.